Introduction

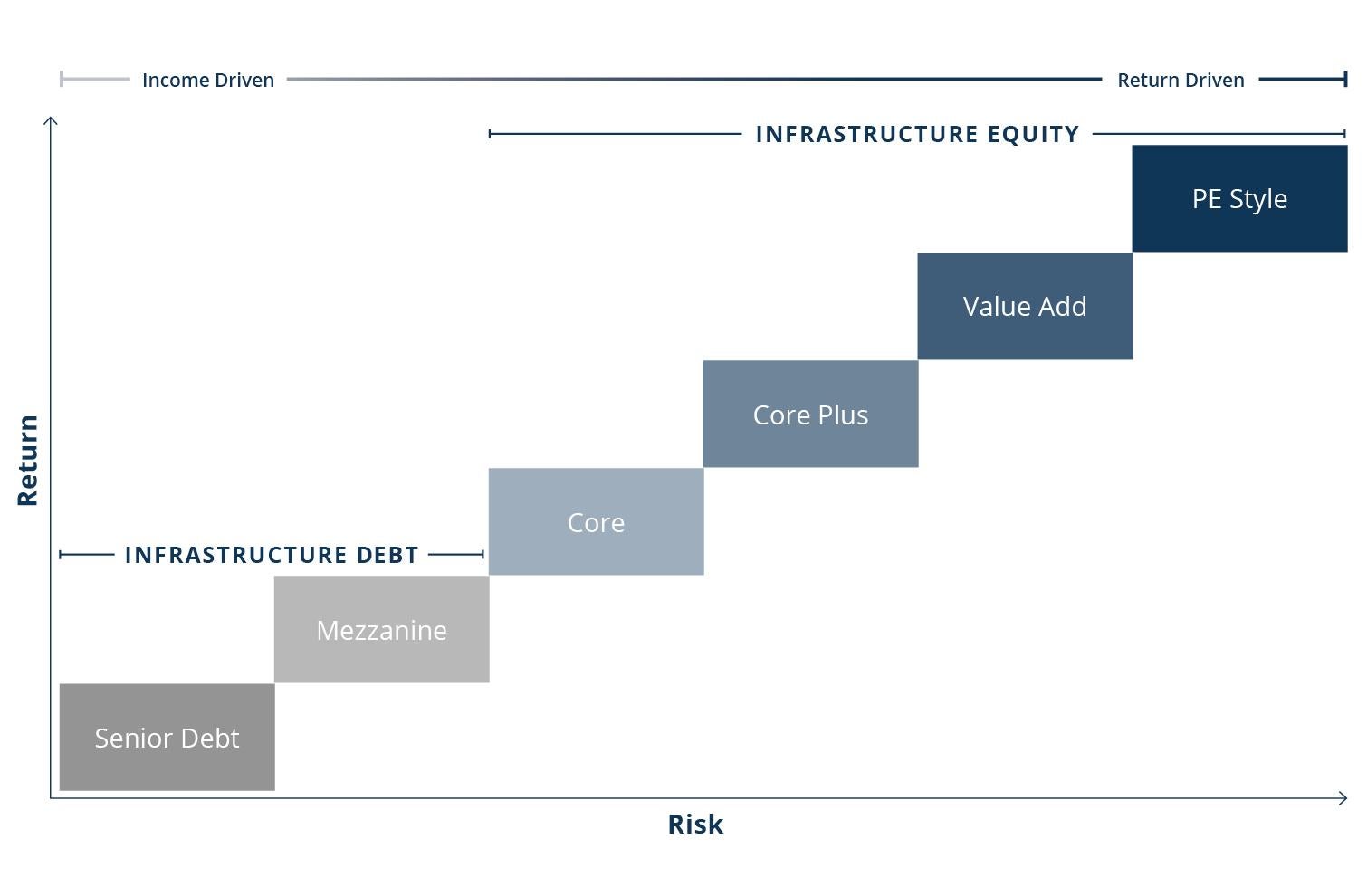

As allocations to infrastructure have grown, many investors have become familiar with the labels used to describe these investments, including “core,” “core plus” and “value add.”

Yet unlike other private market asset classes like real estate, where there is a consensus on the classifications of these risk profiles, the various categories of infrastructure are less precise, and significant differences are often found in how these labels are used.

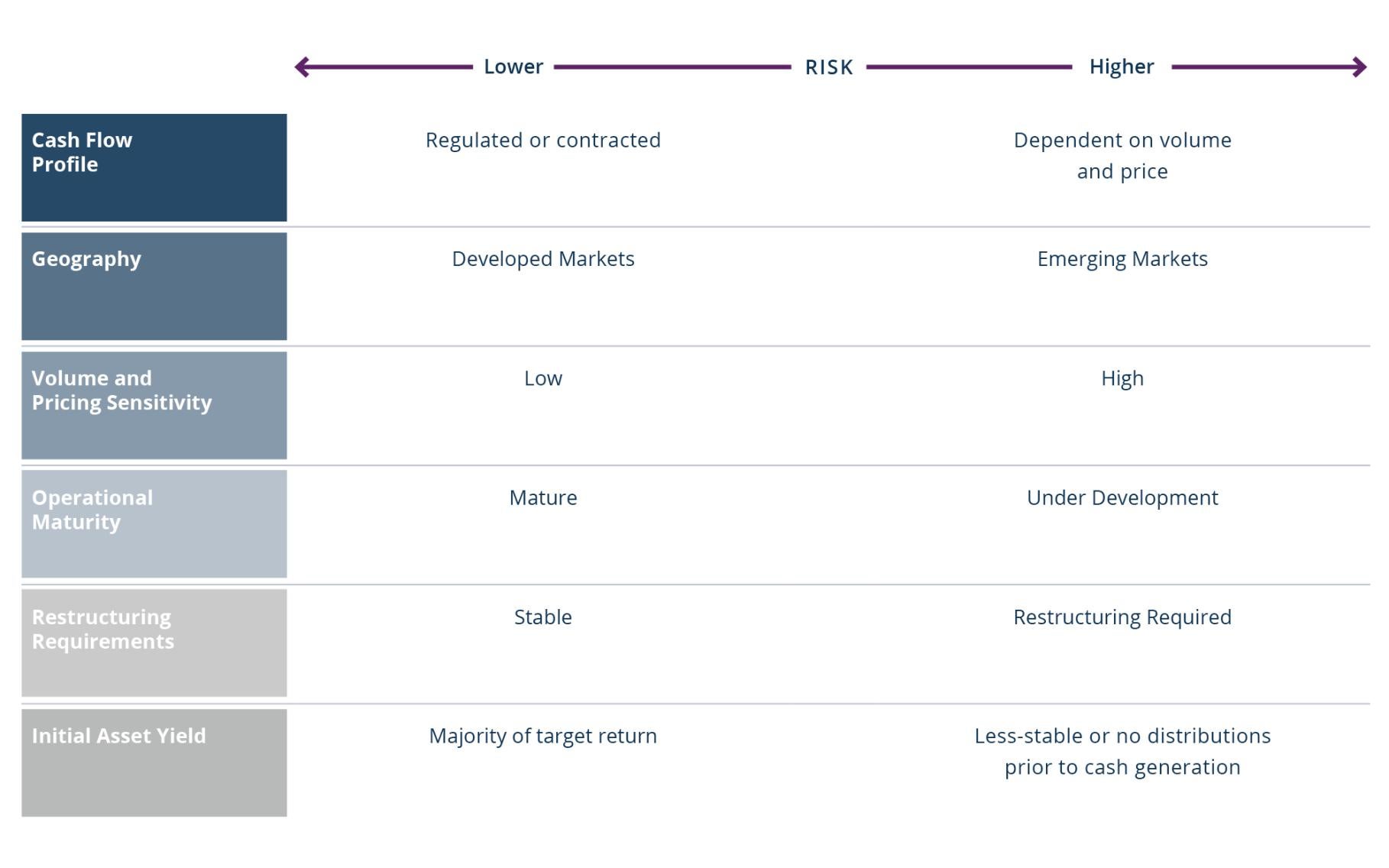

As an asset class, infrastructure has proven its resilience throughout market cycles. However, periods of market volatility have highlighted how these risk profiles can be misleading—and have served as a reminder that not all infrastructure is created equal. The cash flow stability and performance of some assets classified under the same risk profile label have varied during periods of market volatility. And, depending on the magnitude and nature of the variability, value may have been affected as well.

Today, many infrastructure managers describe their investment strategies as core, yet the target gross returns they state can range from less than 8% to over 15%. Clearly, they cannot all have the same definition of core.

Investors, therefore, should not rely on these labels and assume that one strategy’s definition of core is the same as another’s. Instead, they must dig deeper to truly understand the underlying risk profile of a particular strategy (see Figure 1). This is especially relevant in today’s low interest rate environment, where some institutional investors have shifted allocations from fixed income to core infrastructure.

Brookfield invests across the infrastructure risk spectrum, and defines core as investments in lower-risk essential assets with long-term visibility of cash flows. It also includes specific attributes that make the investments resilient in most economic environments and should produce strong-risk adjusted returns.