Introdução

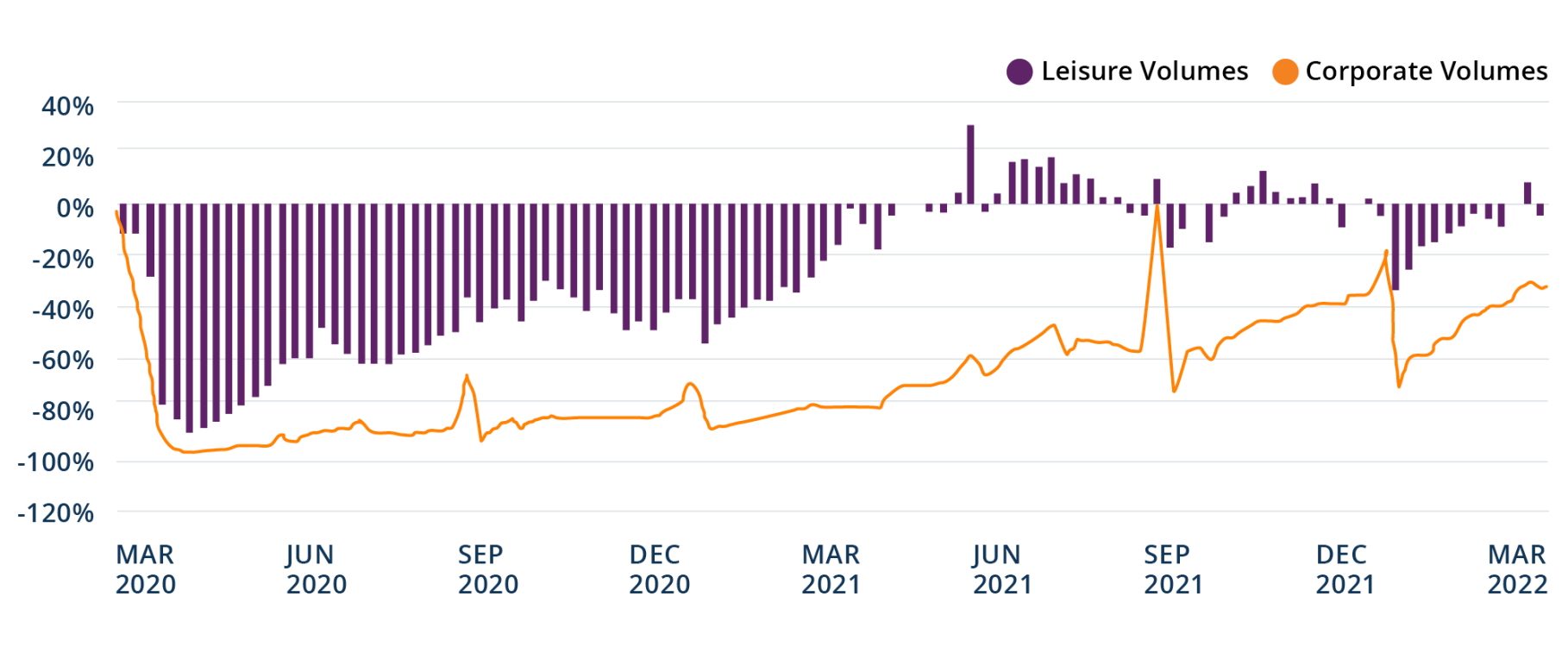

O fluxo constante de notícias sobre os gargalos da cadeia de suprimentos evidenciam a natureza essencial da infraestrutura de transporte e dos ativos logísticos em todo o mundo.

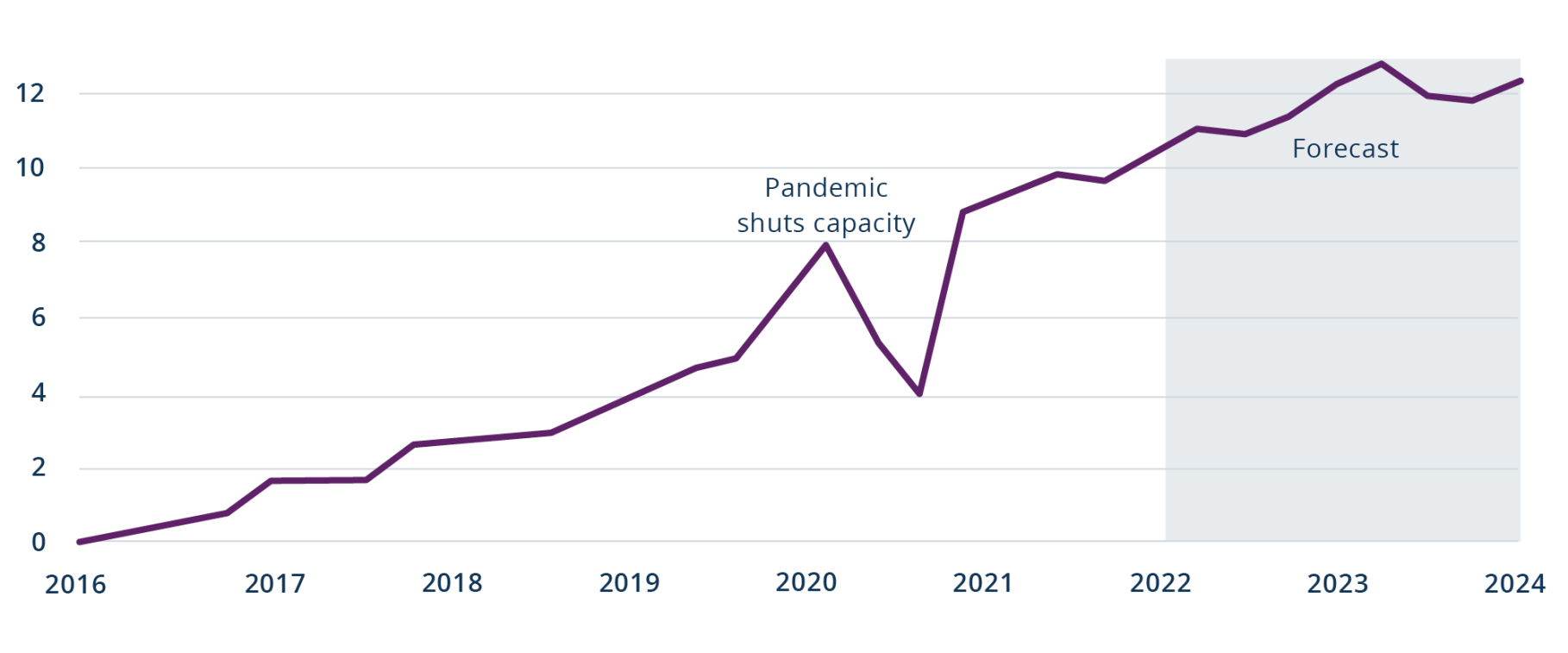

Embora o ápice da disrupção da cadeia de suprimentos provavelmente já tenha passado, ela expôs problemas que persistem, como infraestrutura obsoleta e capacidade, flexibilidade e eficiência insuficientes.

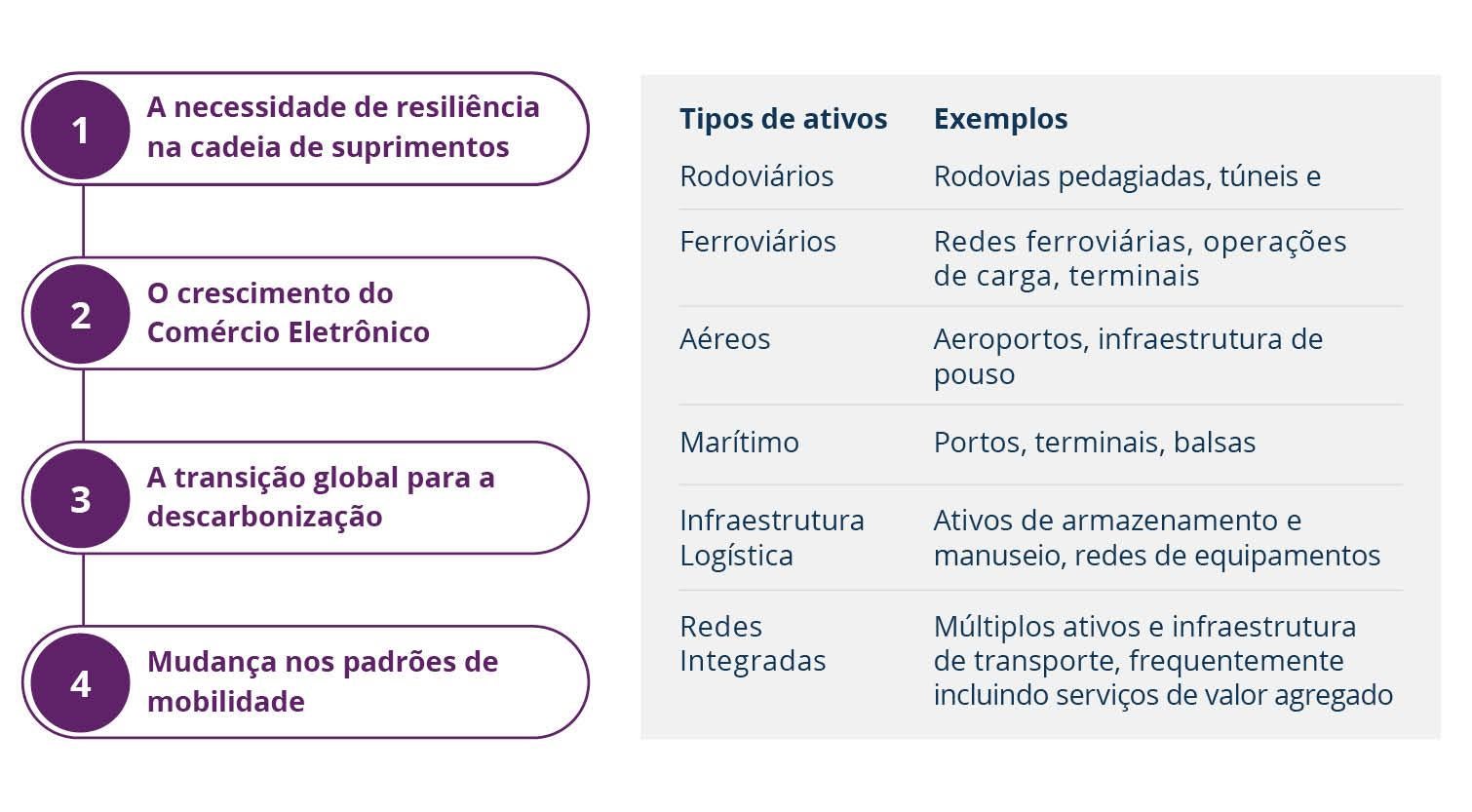

No entanto, a resiliência das cadeias de suprimentos é apenas o primeiro grande tema a ser observado neste universo (ver Imagem 1). Com o crescimento do comércio eletrônico e as mudanças fundamentais na maneira como as mercadorias se movimentam, as empresas de logística de transporte precisarão se adaptar. Essas empresas também precisarão "esverdear" seus ativos e redes para cumprir as metas de redução de emissões de carbono e as regulamentações ambientais emergentes à medida que as iniciativas globais de descarbonização se consolidam. Finalmente, a mudança dos padrões de mobilidade exigirá avanços em tecnologia para permitir novas opções que economizam tempo e são economicamente viáveis, atendendo à evolução das preferências dos passageiros.

Ativos críticos de transporte, como rodovias, ferrovias, transporte aéreo e marítimo, infraestrutura de logística e redes integradas, exigem investimentos significativos para eliminar ineficiências, aumentar a capacidade da malha, descarbonizar e proporcionar maior confiabilidade.

Investimentos são necessários para tornar as cadeias de suprimentos mais resilientes e para atender as mudanças significativas previstas para o e-commerce, descarbonização e mobilidade. Os últimos anos também evidenciaram o papel fundamental das redes de equipamentos de logística nas cadeias de suprimentos globais. Mas, sob a perspectiva de investidor, grandes demandas de capital muitas vezes criam oportunidades atraentes.

Adicionalmente, o cenário atual de inflação elevada e preços aquecidos de commodities ressalta ainda mais a importância fundamental da infraestrutura de transporte para a economia mundial, bem como a necessidade de mais investimentos.