Memos do Mark

Minute Read

I. Introduction

Paul Volcker’s accomplishments and the lessons he bestowed are legion. He is best remembered for his success as Chair of the Federal Reserve in eradicating the high and volatile inflation that plagued America in the 1970s and early 1980s. From that singular achievement, we learned the value of operational independence of monetary policy and the importance of credible and forceful actions to quell high inflation and anchor inflation expectations.

Many of Paul’s other contributions sprang from his deep understanding of the interdependencies within the economic and financial systems. Throughout his career, he was a tireless advocate of improving international cooperation to promote monetary and financial stability. From his time at the helm of the US Treasury and the Federal Reserve Board, he understood how the relationship between monetary and fiscal policies could be virtuous or vicious. From his spells at the NY Fed and in private finance, he knew first-hand how financial markets could anticipate and reinforce credible policies.

Paul understood that financial markets need consistent, comparable and decision-useful disclosure to do their job. That’s why he became the inaugural Chair of the IFRS Foundation Trustees and shepherded in the first uniform global accounting standard. And finally, Paul foresaw the enormous threats from climate change. Never one to avoid tough choices, he was an early and vocal advocate of a carbon tax.2

Today, I will draw on this legacy to consider the macro-economic challenges of the next decades. Economic history is rhyming with alarming force and frequency. The economic environment is now very different from that which reigned since the global financial crisis. Deficient demand and divine coincidence are out, trade-off inducing supply shocks and malign coincidence are in.

I will argue that the policy responses to these developments cannot be considered in isolation of climate change. Indeed, whether it is addressed or ignored, climate change is now macro critical, and climate policy has become the third pillar of macro policy. The conduct of climate policy will directly impact the efficacy of fiscal and monetary policies, and its interactions with the financial system will heavily influence the pace of job and wealth creation. Like the rate of inflation, the degree of climate change is a choice, one that affects the prosperity and welfare of all. On climate change, as with the Volcker disinflation, now is not the time for half measures.

II. Climate Change Is Macro Critical

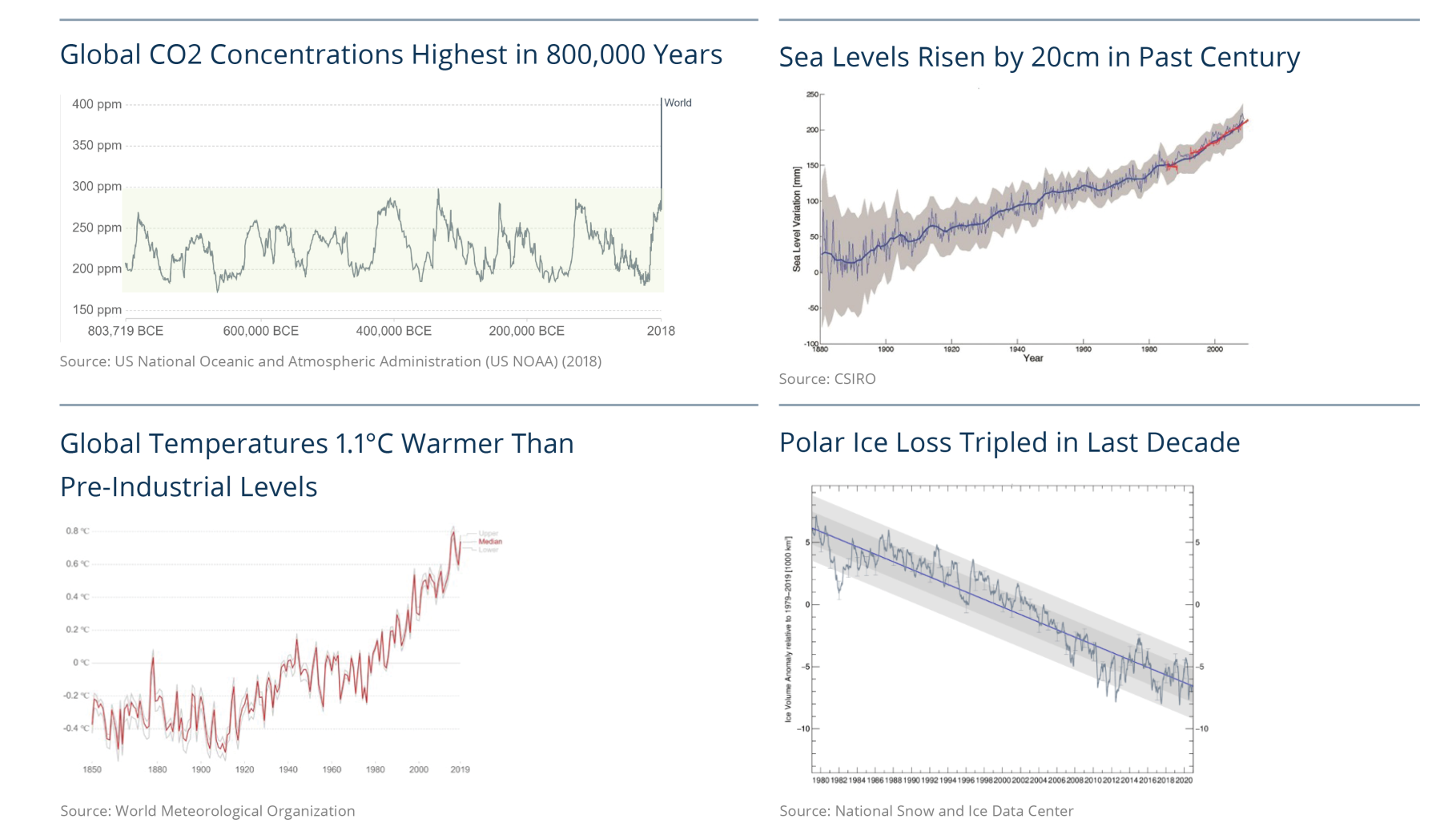

Our planet’s average temperature is already 1.1° Celsius warmer than pre-industrial levels, and the last seven years have been the warmest on record.3 The impacts on our planet’s finely tuned ecosystems are escalating. Our oceans are becoming much more acidic, sea levels are rising and the pace of polar ice loss is accelerating (see Figure 1). Extreme climatic events—hurricanes, wildfires and flash flooding—are multiplying.

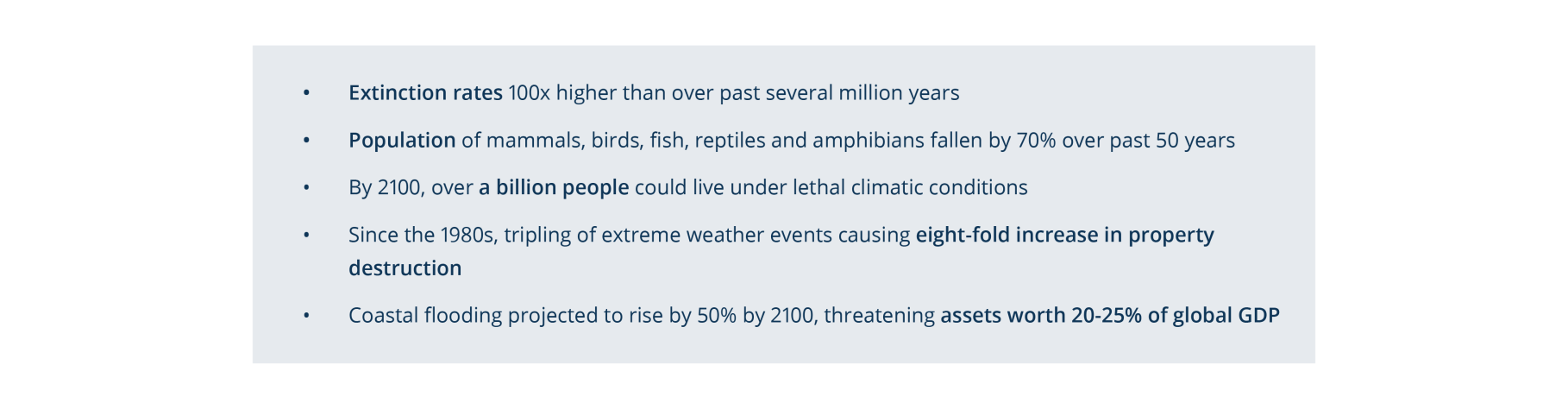

These changes are not only eliminating individual species but also destroying entire habitats such that the population of mammals, birds and reptiles has fallen 70% since I was born (see Figure 2). What had been biblical is now commonplace.

Figure 1: CO2 Emissions Driving Global Temperature Rises, Rising Sea Levels & Polar Ice Loss...

Figure 2: ...With Widespread Impacts

Perhaps because they were not financially valued, these losses in nature were downplayed, and their cause treated as an issue for another day. But now the effects of climate change are beginning to affect assets which have market prices, making the scale of the calamity more tangible.

I know from my time supervising the world’s fourth-largest insurance industry that since the 1980s, the number of extreme weather events has tripled, causing an eight-fold increase in insured property destruction.4 An even greater value of assets is uninsured, with the global protection gap reaching a record $104 billion in 2020.5 These losses are expected to rise sharply, with coastal flooding projected to increase by 50% by the end of this century, threatening assets worth one quarter of global GDP.6 In parallel, the livelihoods and lives of over a billion people will be directly affected by the spread of lethal climatic conditions.

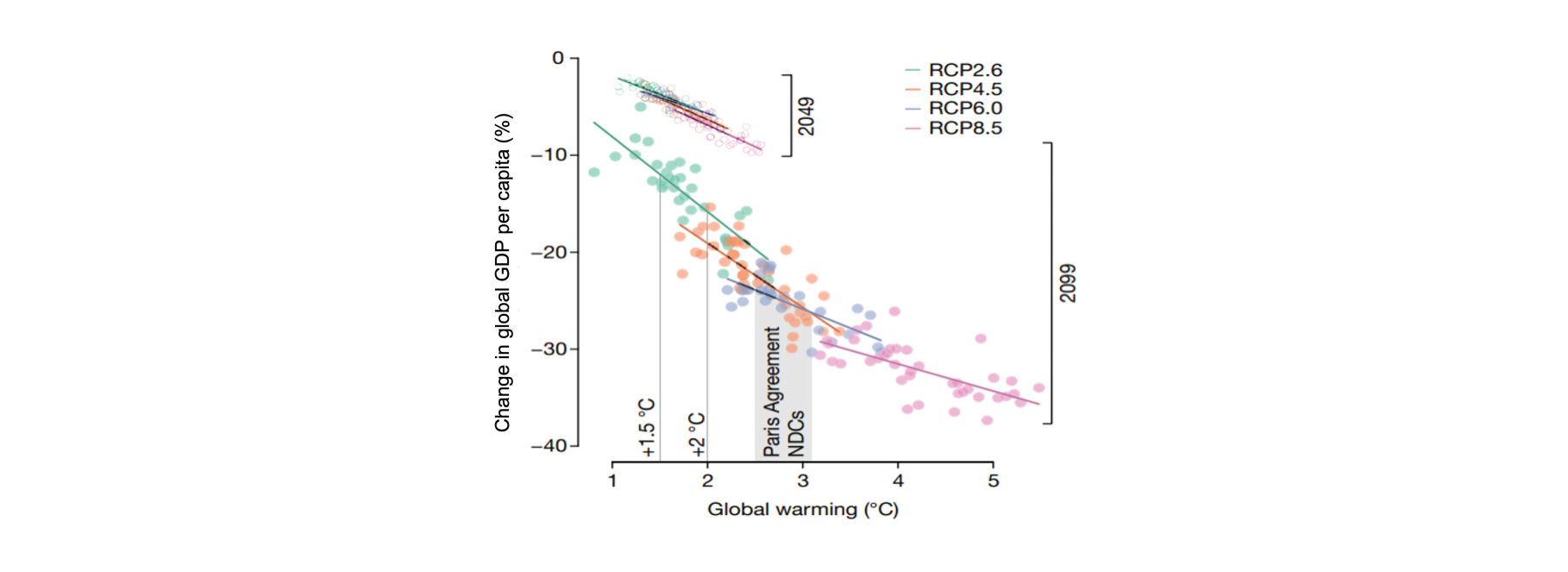

Insured losses measure the value destruction of the stock of assets. GDP measures the flow of income. Estimates suggest that, over the balance of this century, climate change could cause the equivalent of a decade of no economic growth (see Figure 3). Of course, GDP represents a single year’s worth of value added in the economy. In general, estimates of the impact of climate change project that what is lost is likely to stay lost, making climate change the curse that keeps on taking.

Figure 3: Temperature Impacts Alone Could Drive a Lost Decade of Growth

Under different RCP forcing scenarios, relative to a no-warming baseline (SSP1). The three vertical black lines denote the 1.5°C target, the 2°C target and the median-estimated warming expected under current Paris commitments (2.9°C). Source: Burke et al

As significant as these figures are, it is instructive to think of what is not included in them, both those assets outside the market economy—such as biodiversity and human health—and economic channels not modelled, including disrupted supply chains and the very real challenges to monetary and financial stability that climate change will present.

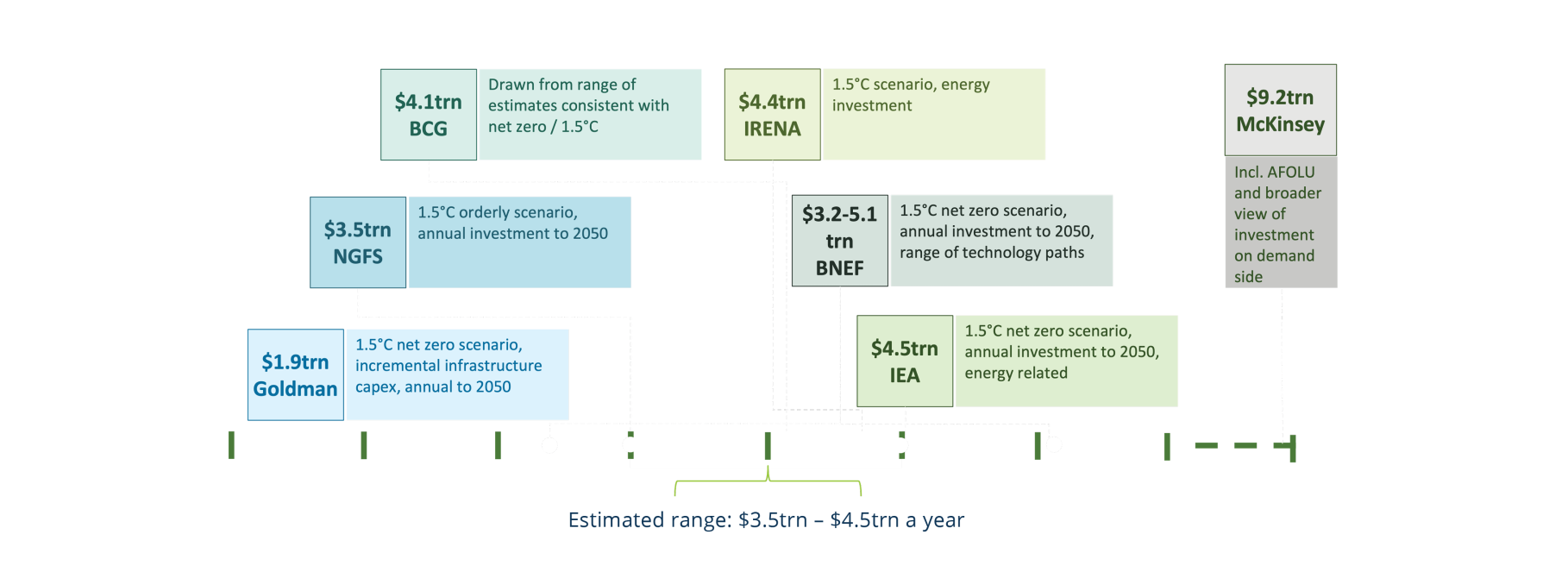

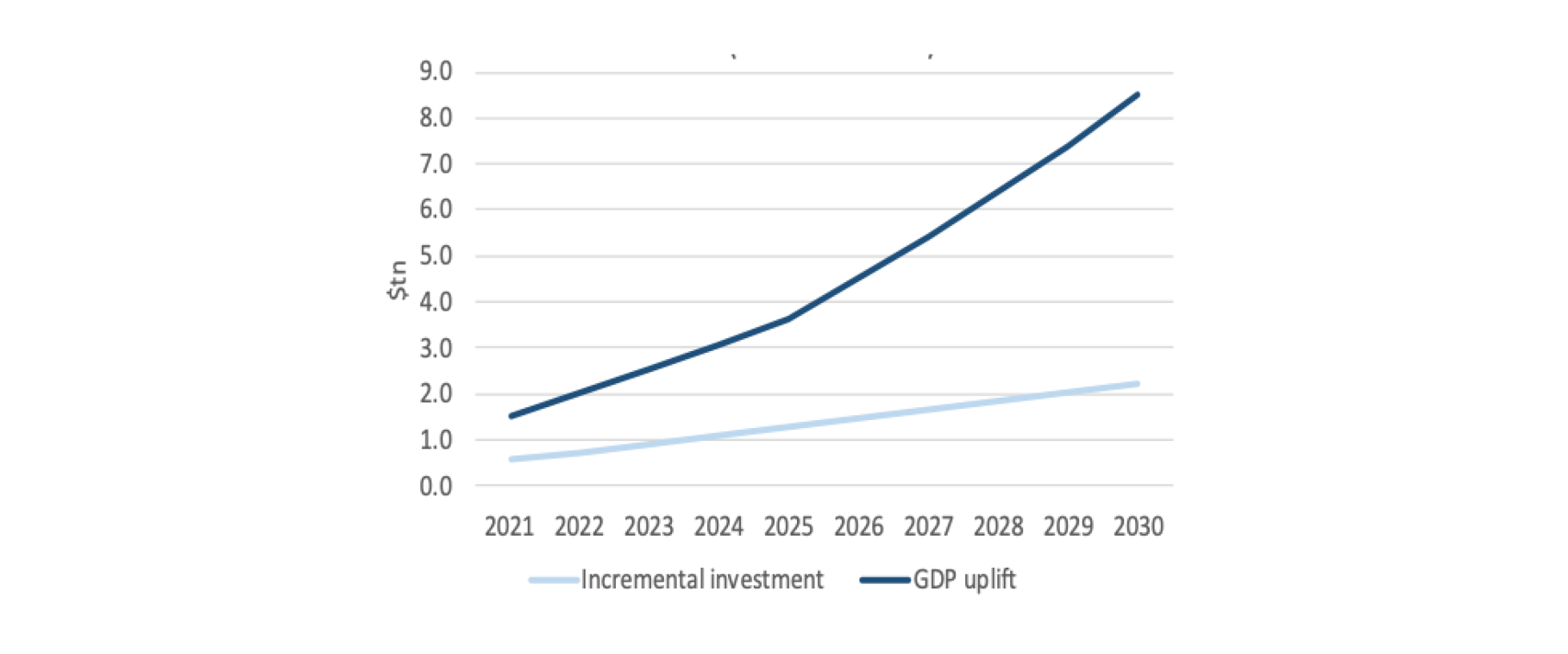

Lest this quick summary appear too gloomy, let me balance it with the macro-economic upside from addressing climate change. In particular, the net-zero transition represents a multi-decade investment boom after a decades-long drought. Although estimates vary depending on whether they focus on the energy transition, broader industrial restructuring, or the full range of investments to adapt our infrastructure and build resilience for a warmer and more volatile climate, even in the most limited cases, they are enormous (see Figure 4).

At the lower end of the spectrum, the IEA (2021) calculates that to be on track for 1.5° warming, global investment in energy infrastructure alone must rise from 2.5% of world GDP in 2016-20 to 4.5% by 2030, before gradually returning to 2.5% by 2050.7 Arguably in a more fragmented energy market where security concerns have become paramount, the figures will be even higher.

The product of this investment is a secure and sustainable energy system, carbon-competitive economies, more jobs and higher growth. With respect to the last, the IEA forecasts material GDP multipliers, with global output that is more than 4% higher by the end of this decade (see Figure 5).

Figure 4: Annual Investment for Net-Zero Transition Needs to Double to ~$4trn…

Figure 5: …Bringing Significant GDP Multipliers

GDP uplift from incremental investment in the net-zero transition (IEA, IMF)

Under IEA net-zero scenario, every $1 of net-zero investment results in over $3 of additional GDP

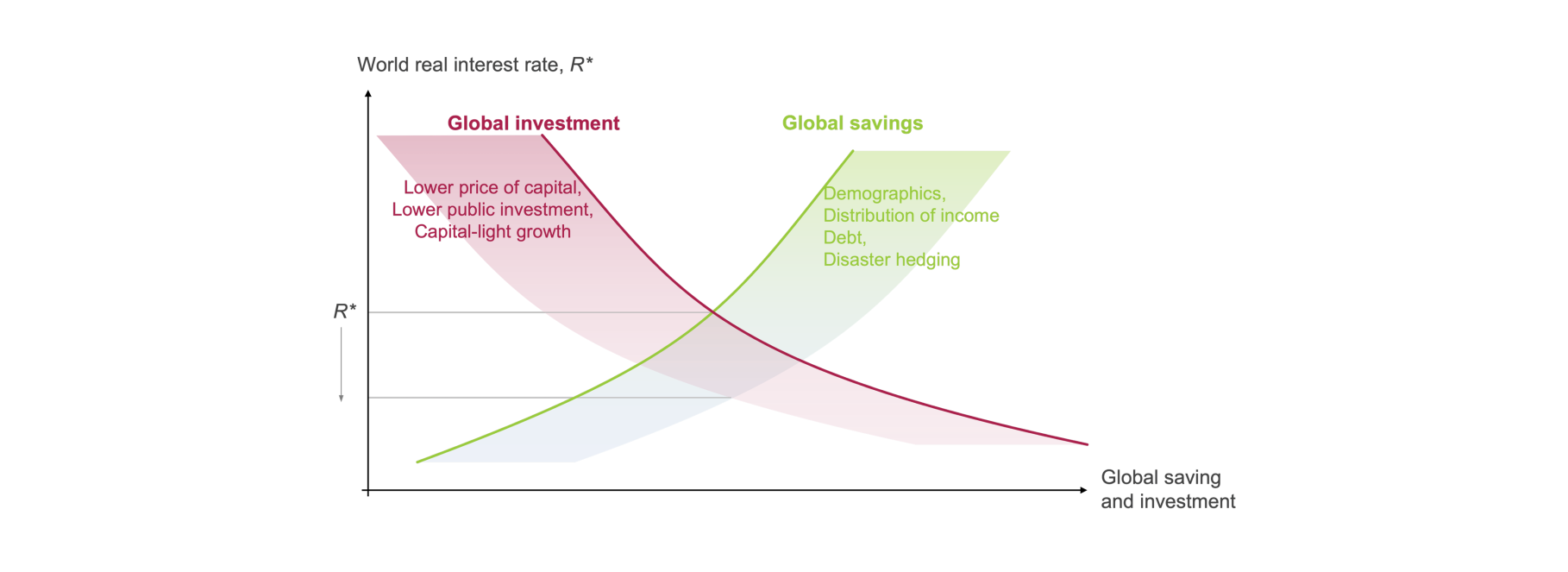

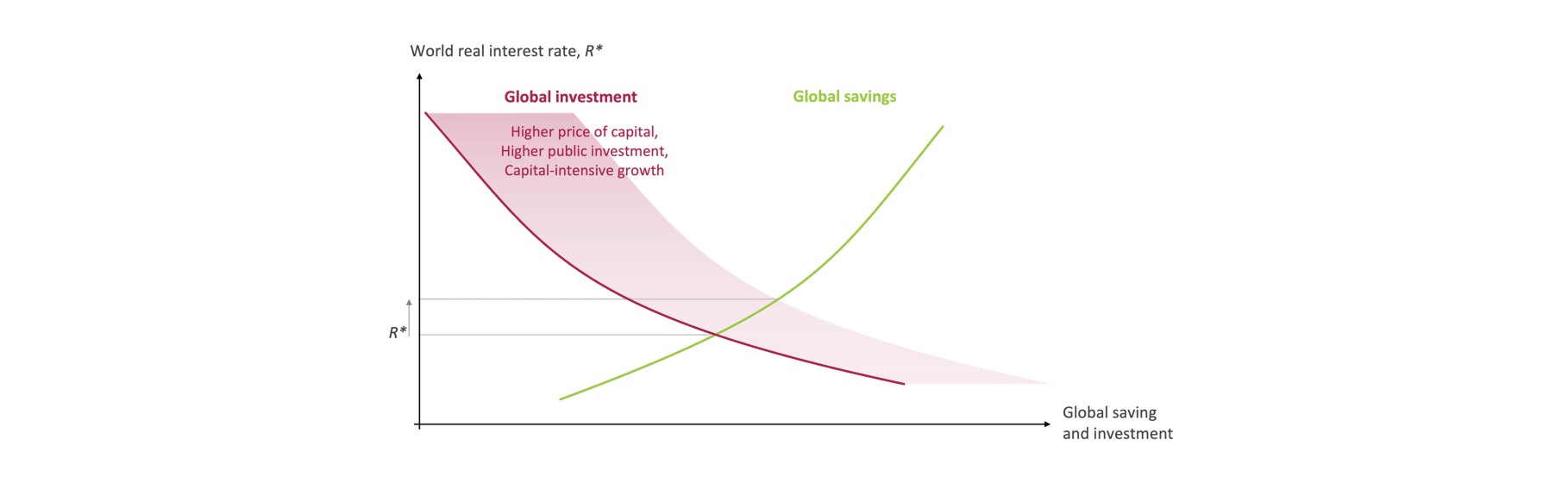

Investment on this scale would completely offset the investment shortfall (the twin of the savings glut) that has emerged this millennium (see Figure 6).8

All else equal, this would increase the equilibrium real interest rate, r*, thereby reducing the risks of monetary policy being trapped at the effective lower bound and raising both the path and terminal values of monetary policy rates consistent with price stability (see Figure 7).

Figure 6: Transition Investment Would Offset Some of the Structural Changes That Have Lowered R*...

Figure 7: ...And Would Reverse the Investment Drought and Raise R*

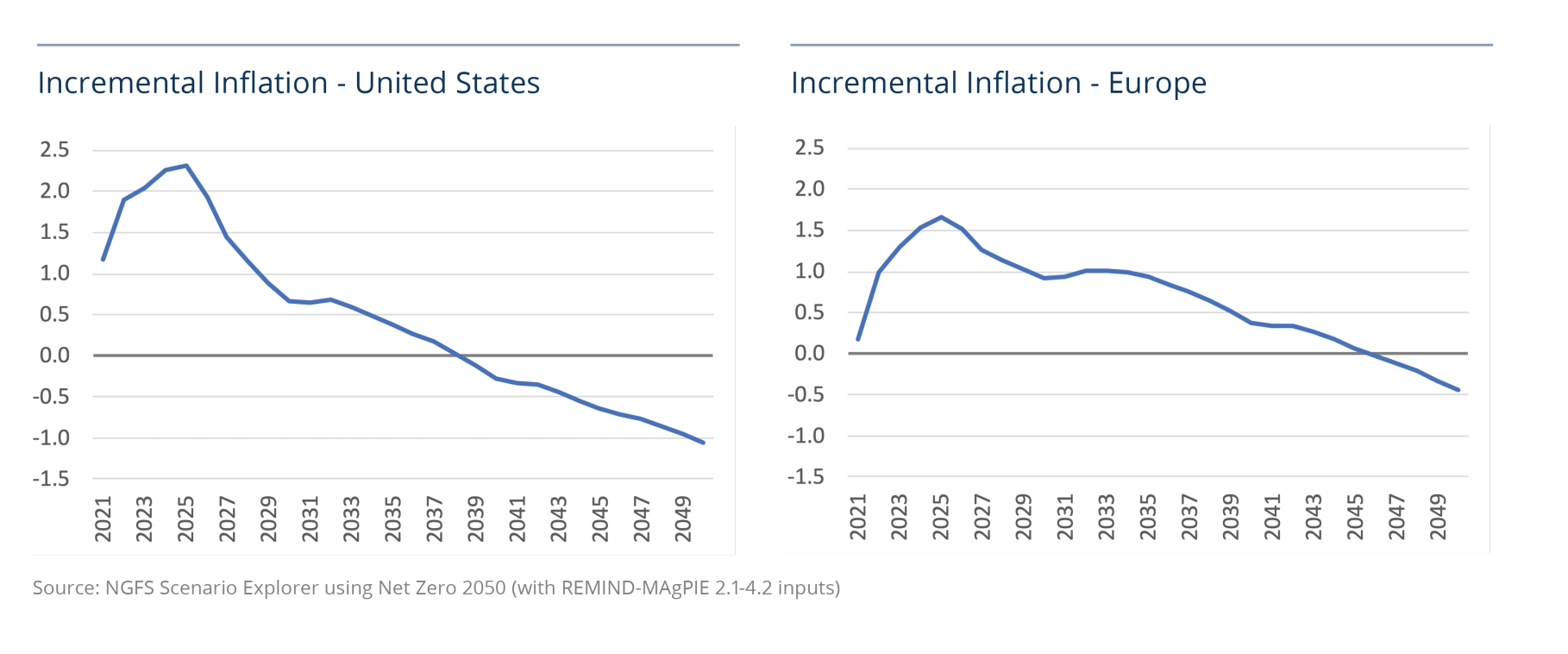

Which brings me to the inflationary impact of climate change, starting with the impact of a transition to a net-zero economy consistent with limiting temperature rises to 1.5°.

While fundamentally positive and likely to be less inflationary than keeping with current insufficient climate policies, the net-zero transition can be expected to put upward pressure on inflation during the initial decade of the transition, until the lower levelized costs of clean energy weigh on prices thereafter.

The most important inflationary impact of the transition is that it constitutes a major supply shock that affects virtually every sector of the economy in every region. On a simple comparison, it is on the same order of magnitude as the oil shocks of the 1970s which rendered large swathes of the economy uncompetitive and triggered the inflationary spiral that Paul Volcker eventually had to vanquish.9

Of course, unlike the oil shock, the price impact of the net-zero transition will be spread over years rather than concentrated in a few months. Analysis by Jean Boivin et. al. (2022) straight-lines this increase over the next decade, implying a notable 40 basis point impact on annual inflation.10

In the more comprehensive NGFS modelling, the annual inflation impacts are large, ranging between 100-200 basis points in the US in the first half decade, before fading and becoming deflationary as the greater cost competitiveness of clean energy takes hold. The impacts in the less-energy intensive Euro area are smaller but still macro significant (see Figure 8).

In the models, policy rates do not match the increase in inflation given the trade-off (i.e., real rates fall). Crucially, inflation expectations are assumed to remain well anchored as monetary policymakers draw on a seemingly infinite reservoir of credibility. Paul Volcker’s legacy is large, but central bankers should remember that even the most generous bequests can be exhausted. This is especially true since the net-zero transition will be only one of several supply shocks our economies face in coming years.

Figure 8: Net-Zero Transition Is Likely Inflationary Near Term/Deflationary Long Term

‘Shadow’ carbon pricing creates near-term upward pressure on inflation

III. A World of Supply Shocks

The global economy is undergoing a series of major transitions with significant implications for macro-economic policy and asset prices. The long era of low inflation, suppressed volatility and easy financial conditions is ending. It is being replaced by more challenging macro dynamics in which supply shocks are as important as demand shocks, increasing inflation, volatility, interest rates and risk premia.

Covid may prove the last battle of the last war. With the first severe lockdowns, the economic impact fell primarily on demand. Central banks, concerned about the liquidity trap and risks to financial stability, not only massively eased policy but also shifted their reaction functions by committing to sustained overshoots of inflation. This was a tactic—a new tool—in the face of very low r* and a perceived deflationary shock. Considerations regarding the degree of inflation overshooting are now ones of strategy.

In the near term, Covid is moving from pandemic to endemic at different rates in different regions. This will continue to challenge global supply chains given their heavy reliance on Asia. Russia’s horrific invasion of Ukraine is the second massive negative supply shock in two years. The war has accelerated the forces of de-globalisation. Continuing a trend, sanctions have targeted technology and finance. Geo-political risks have ruptured European energy markets. More broadly, companies are building more resilient supply chains and are increasingly engaged in geo-strategic onshoring. The resulting fragmentations of the global system will increase domestic security, while raising costs and increasing economic volatility.

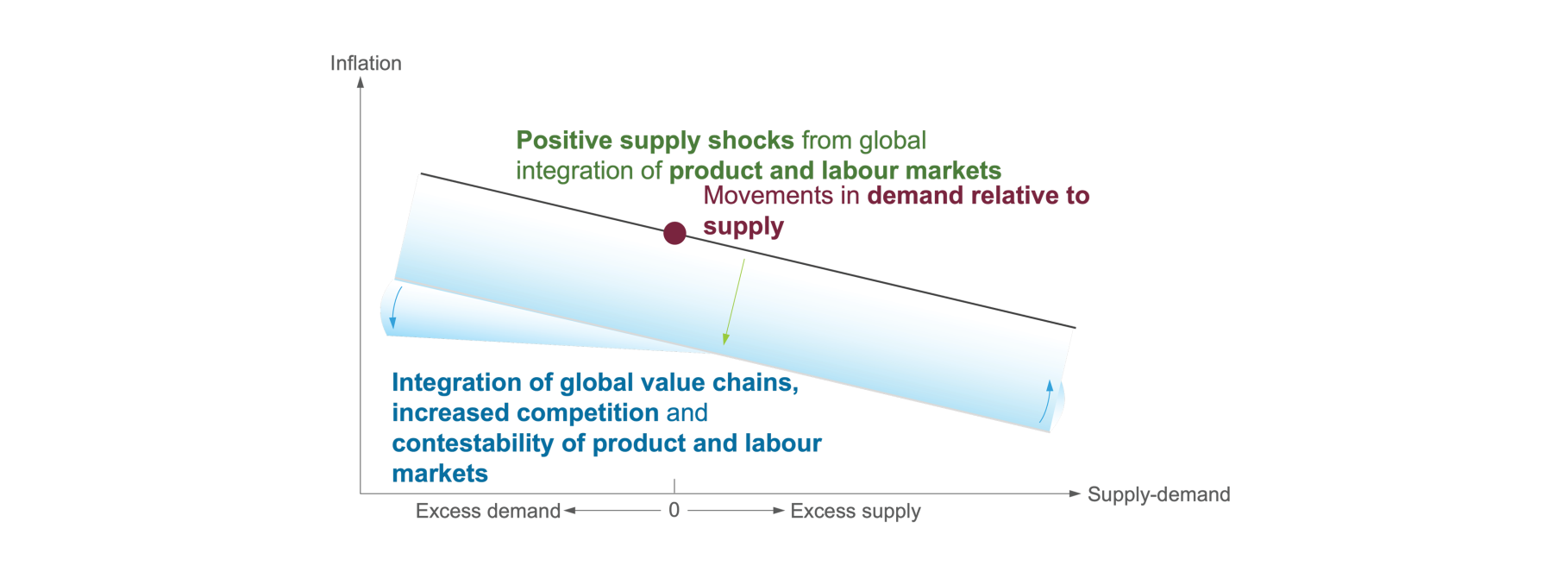

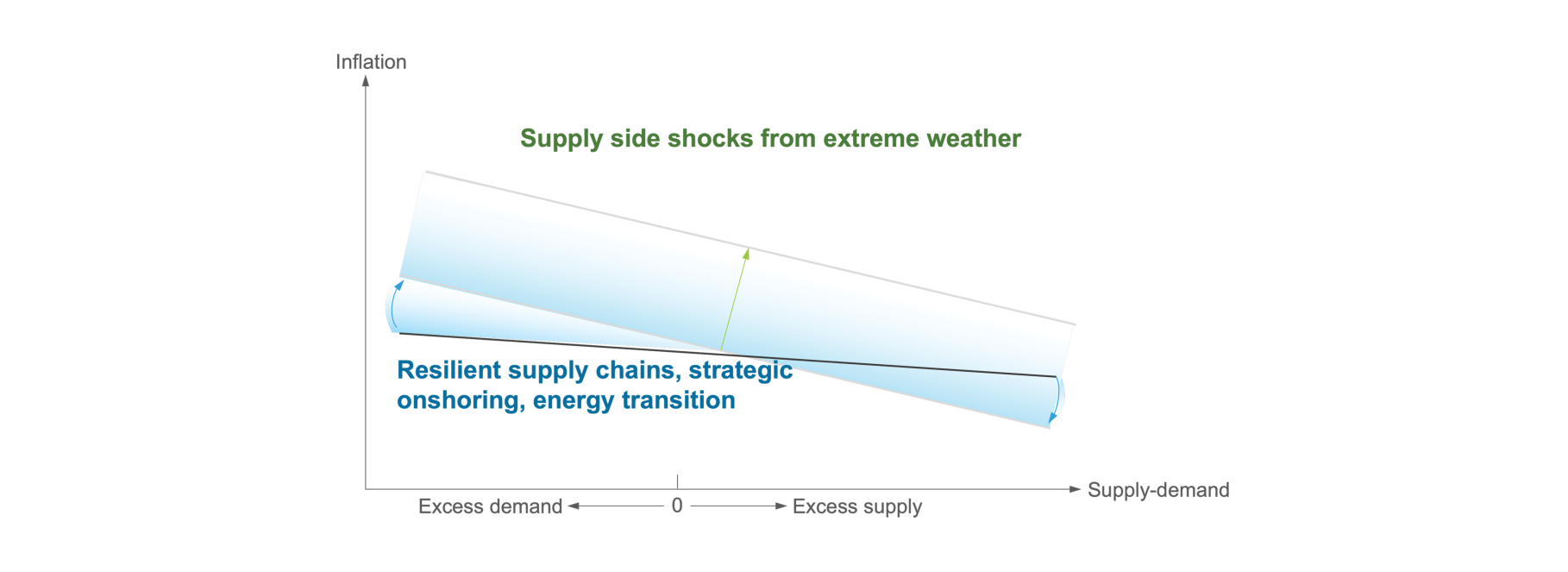

Just as globalisation was deflationary, its unwinding will be inflationary (see Figure 9).11 This is a new environment for monetary policy.12

Figure 9: Globalisation Has Delivered Persistent, Positive Supply Shocks...

...But De-Globalisation and Climate Will Reverse This Trend

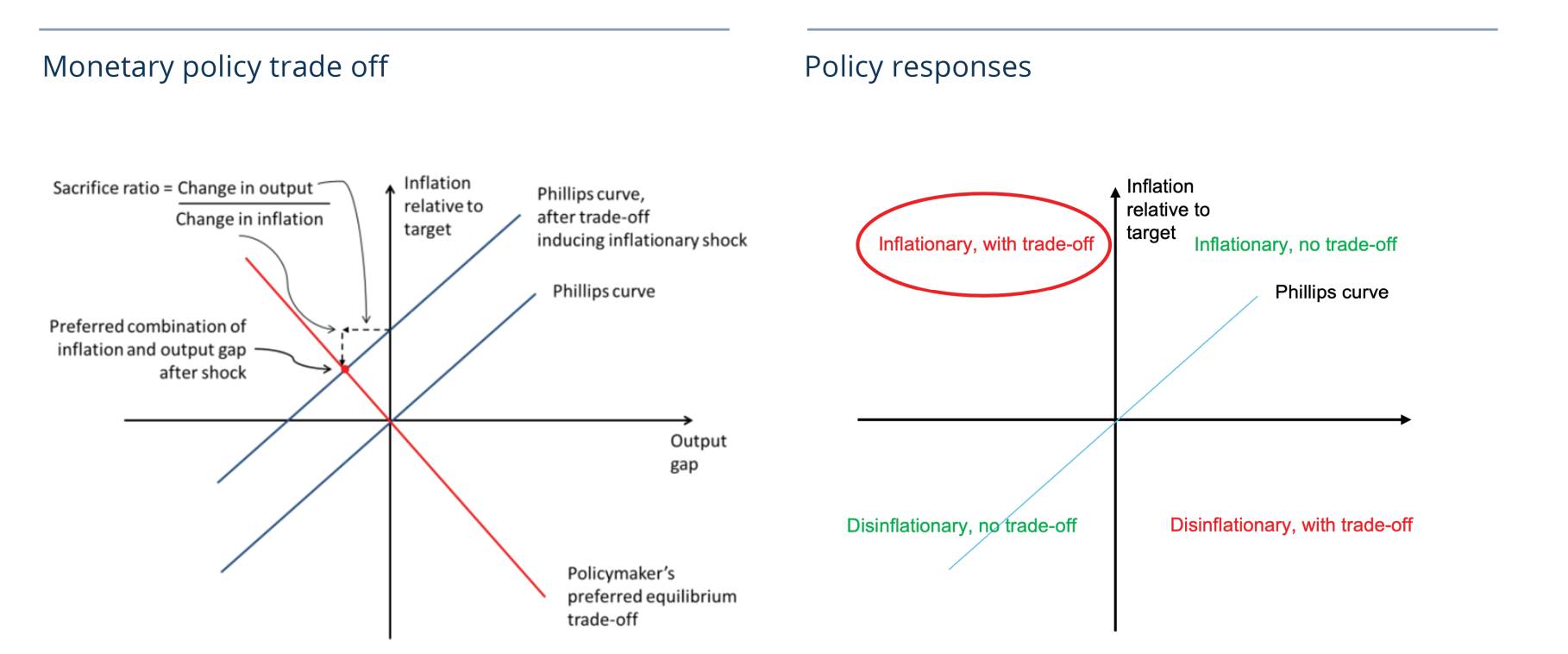

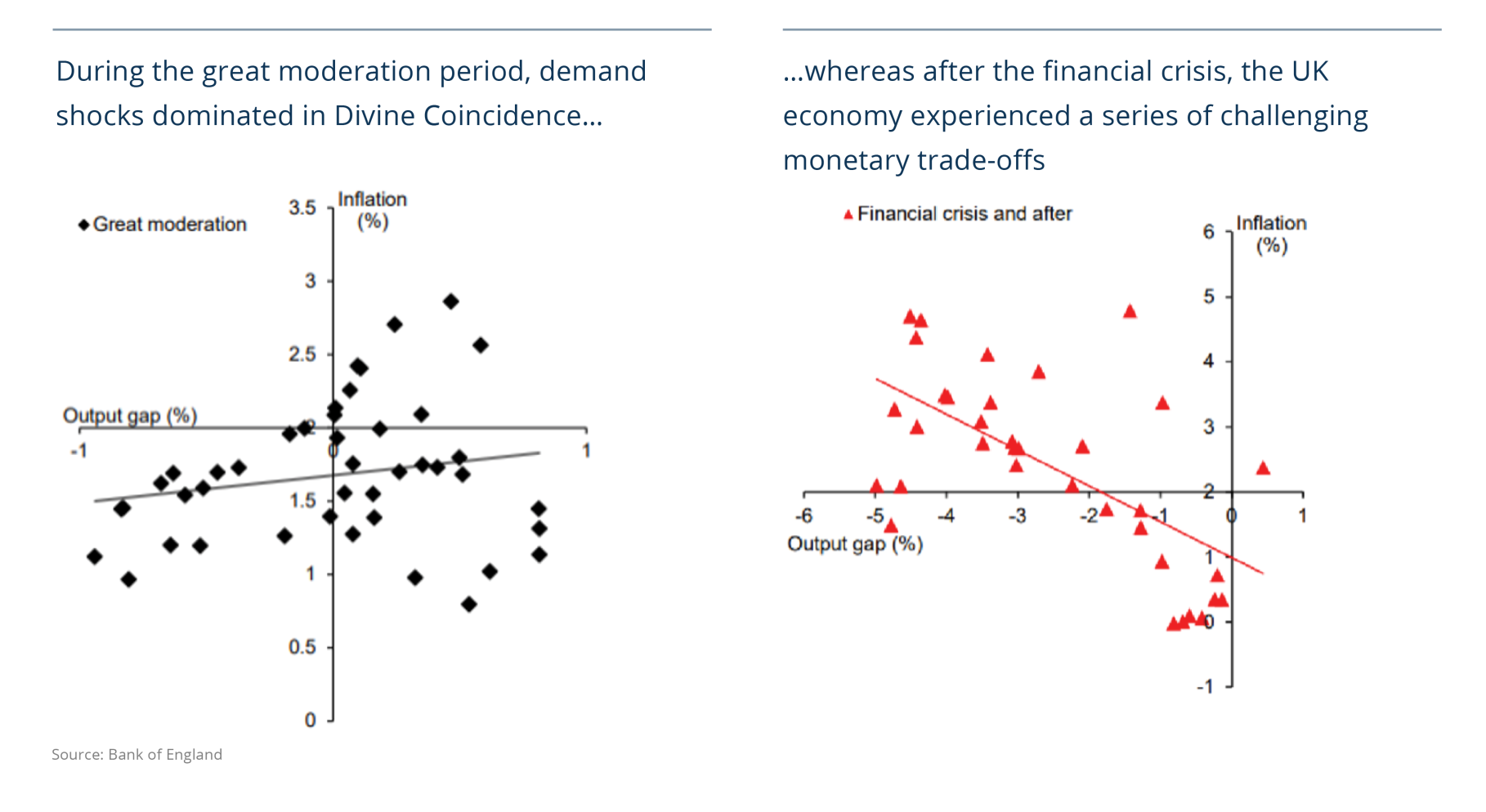

Shocks to aggregate demand drive inflation and output in the same direction. These can include variations in government consumption, households’ desire to consume, or business’ desire to invest. Because monetary policy influences demand, it can lean against such shocks and stabilise inflation. In this case, no output-inflation trade-off arises under so-called “divine coincidence” (see Figure 10).

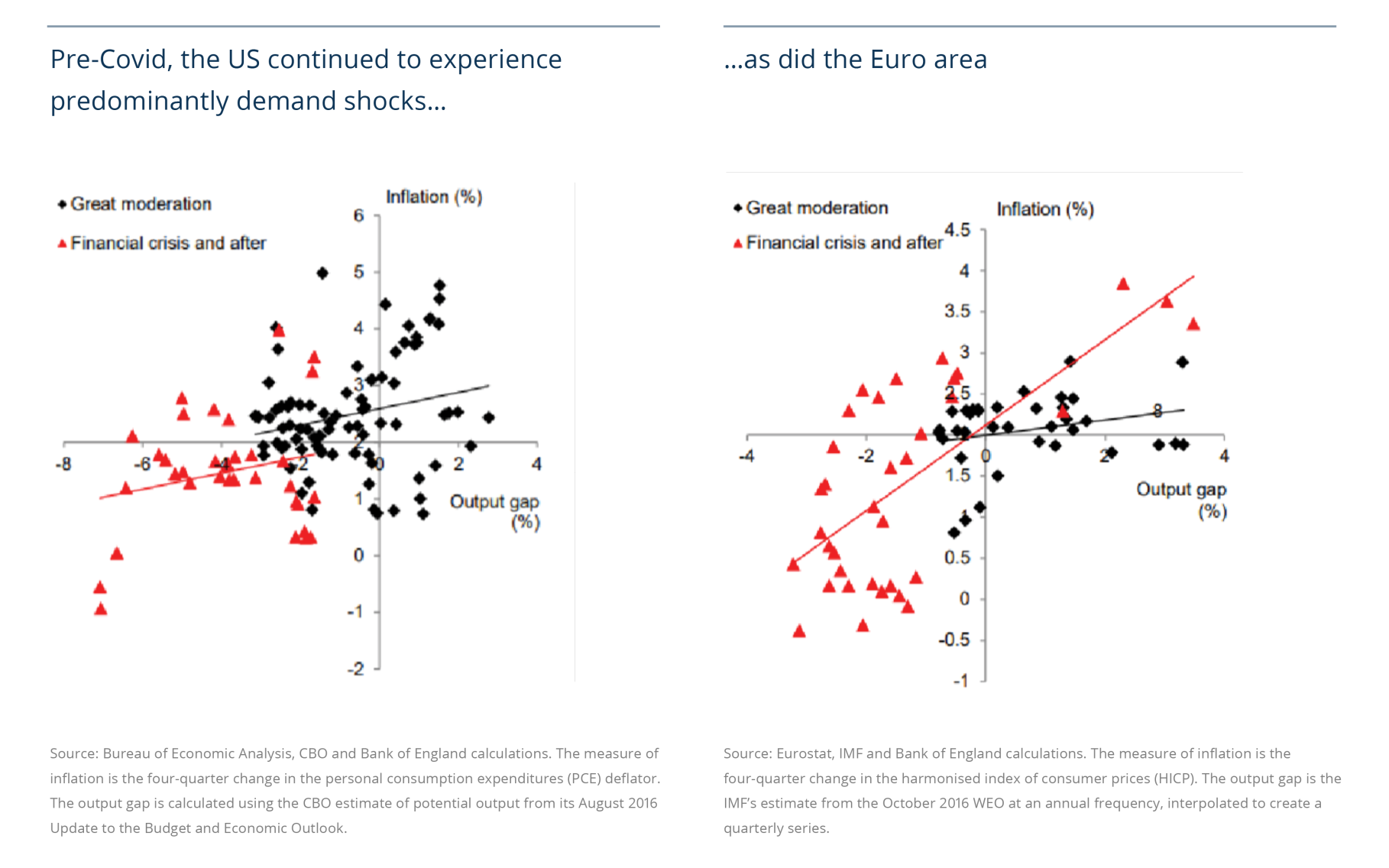

That was the case prior to the global financial crisis for all major economies and for the period between the global financial crisis and Covid for the US and EU (see Figure 11).

Things are different when shocks drive inflation up or down independently of demand. Shocks to the exchange rate, commodity prices or the economy’s supply capacity also have similar characteristics. Because monetary policy’s influence on inflation is predominantly indirect, via demand, in such circumstances inflation can only be controlled by causing a reduction in spending via higher interest rates.

Since the global financial crisis, major central banks have generally faced “divine coincidence” in which low inflation and persistent underemployment both demanded highly accommodative monetary policy. This pushed term premia negative, lowered long-term interest rates and suppressed volatility across asset classes.

Figure 10: From Divine Coincidence to Tough Trade-Offs

Figure 11: US and Euro Area Haven’t Had to Grapple With This Shift...Until Now

The UK was not as fortunate, facing a series of financial, exchange rate and trade shocks, which necessitated striking trade-offs (see Figure 12).

Now all major central banks are facing a series of negative supply shocks. The textbook response is to accommodate it through above-target inflation for a period13 to facilitate the reallocation of resources across sectors, and ensure supply constraints are less persistent.14

However, pursuing such a strategy without losing credibility will be difficult in the face of persistent supply shocks, especially given the less-than-ideal starting point for inflation. The time for tough choices and policy coordination is at hand. Paul Volcker’s legacy lives on.

Figure 12: UK Policymaking Challenged by Supply Side Shocks Since Global Financial Crisis

IV. Climate Policy Is the New Pillar of Macro Policy

Paul understood the importance of policy coordination, and that, in inflationary environments, fiscal discipline should complement monetary tightening. This will be challenging over the medium term as governments pay a series of insurance premiums to build more resilient economies, including support for the onshoring of technologies and supply chains, and spending much more on defence and health care.

Fiscal support will also be required to help workers re-skill during this series of supply shocks. Given these many demands, fiscal capacity for climate action must be targeted and complemented by clear frameworks that drive private investment and innovation.

This leads to the other vector of policy coordination—climate policy—which is now the third pillar of macro policy. The net-zero transition is disruptive, but this should be a controlled disruption—a transition that is guided by credible and predictable policies so that the private sector can drive investment.

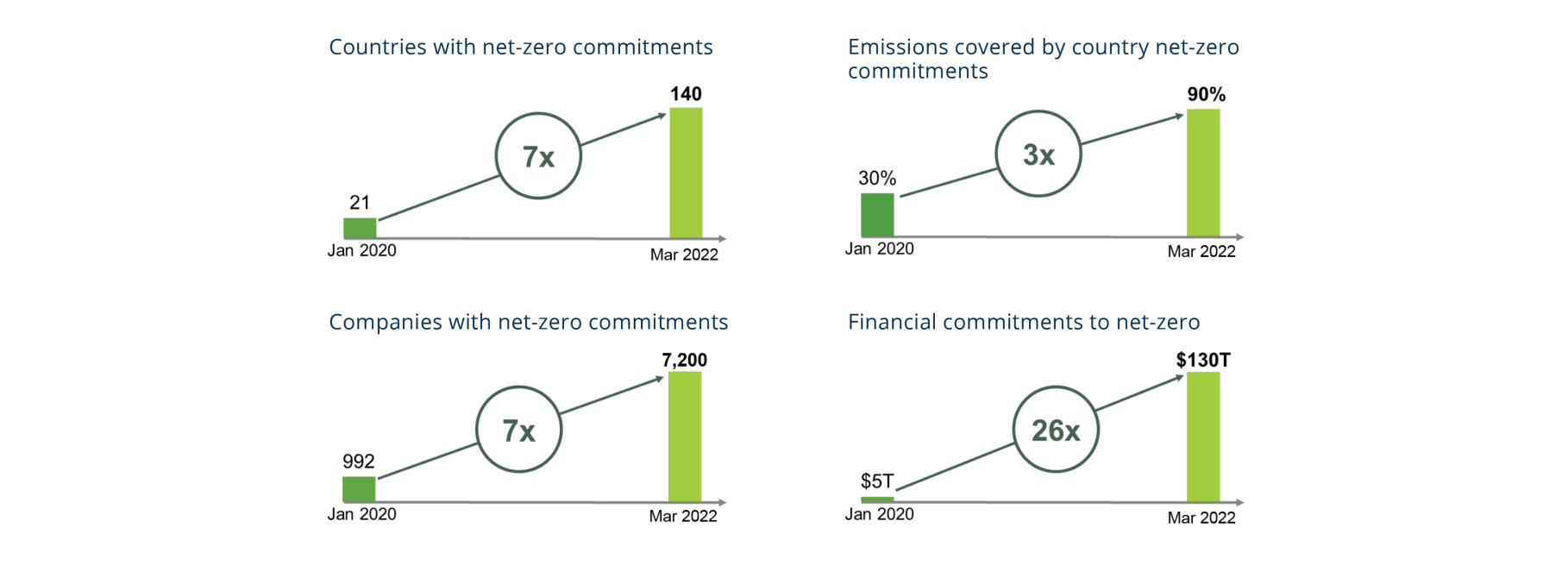

This begins with clear objectives. The foundations were laid at COP26 last November, where the proportion of global emissions covered by country net-zero targets rose from less than one third two years ago to almost 90% (see Figure 13).15 Net zero is now the organising principle for 7,200 of the world’s largest companies, and with the right policies, it will become the norm throughout our economies.

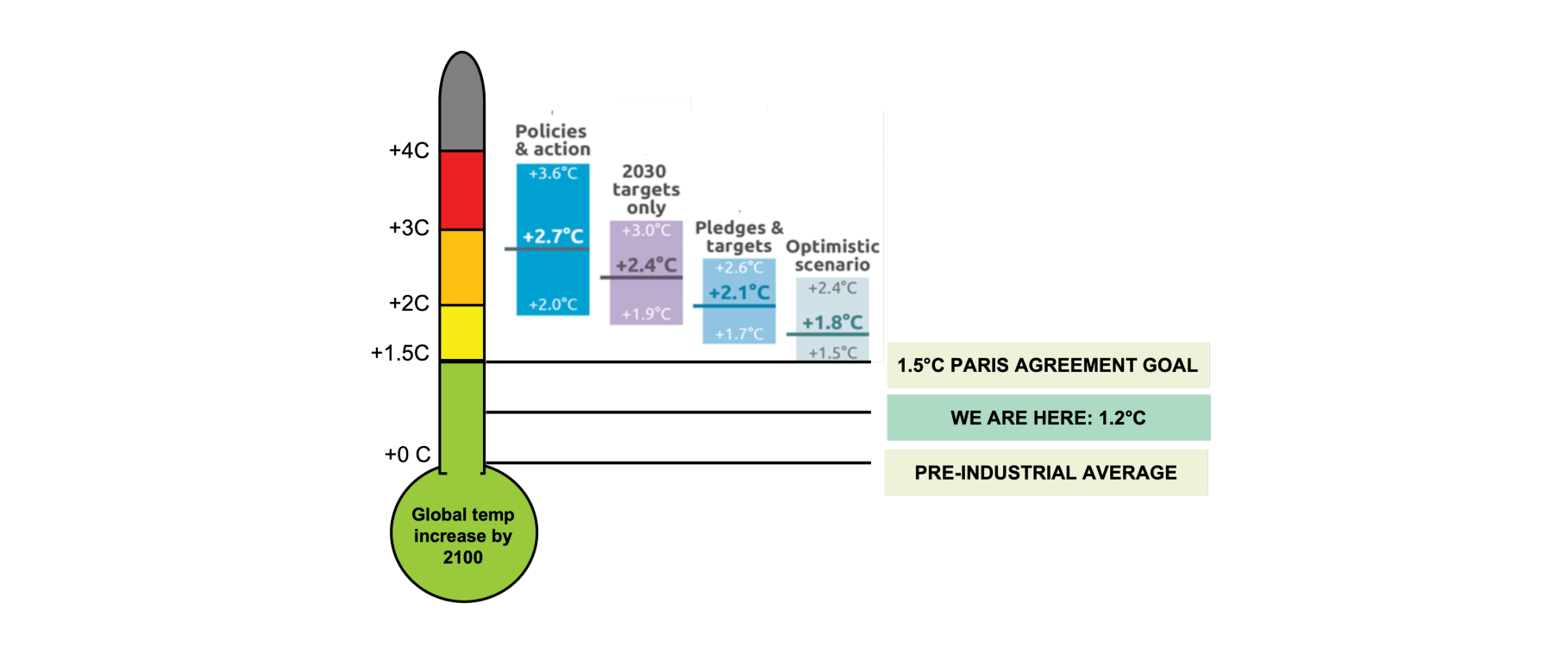

Committing to net zero is, of course, just the start, and there is currently a large gap between ambition and action (see Figure 14).

Governments need to set the terms of, and incentivise, private investment in the net-zero transition. As Secretary Yellen and I have emphasised, the more credible and predictable are government climate policies, the more investors will pour in money in anticipation, creating a virtuous circle of large-scale investment, faster decarbonisation, more jobs and faster growth.16

Figure 13: Net-Zero Transition Accelerating

Sources: Climate Action Tracker, United Nations Climate Change Race to Zero, Glasgow Financial Alliance for Net Zero (GFANZ)

Figure 14: Global Emissions Covered by Net-Zero Targets Rising But Action Still Lagging

Source: Climate Action Tracker

Credible climate policy relies on:

- Broad political support. The experience with inflation targeting demonstrates the importance of politicians across the political spectrum acknowledging the problem and setting clear goals.

- Clear tracking of progress, including “marking to emissions” the carbon budget and clearly identifying gaps in climate policies. A model is independent bodies that assess progress, such as the UK’s Climate Change Committee.

- Building a track record of measures to achieve these intermediate goals. Examples include policies such as the UK and European moratoria on internal combustion engine vehicles from the 2030s and the Canadian legislated carbon price of C$170/tonne in 2030. These future commitments to price the externality of carbon are far enough in the future that companies can act and close enough that they must.

The policy frameworks with the greatest impact will be time consistent (not arbitrarily changed); transparent (with clear targets, pricing and costing); and committed (through treaties, nationally determined contributions and domestic legislation).

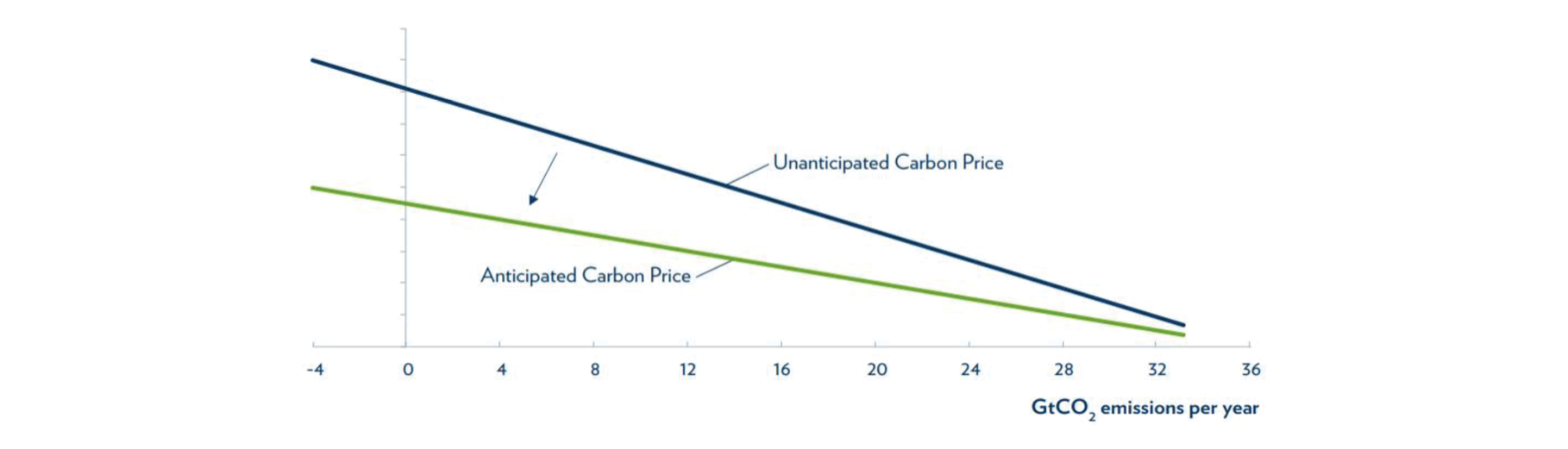

As Paul Volcker’s legacy has demonstrated, policy credibility can do much of the work, lowering the tightening required. If climate policy actions are anticipated, they can be more modest, bringing forward investment, smoothing the transition and lowering the inflationary impacts (see Figure 15). This is Volcker-esque policy coordination that delivers better macro-economic outcomes:

- More investment today with higher GDP and job creation,

- Lower inflation because adjustment and price effects are smoother, and

- Lower emissions and greater energy security.

Figure 15: Credible Climate Policy Catalyses the Financial Sector to Finance Emissions Reduction, Driving Stronger and Smoother Macro-Economic Outcomes

Source: G30 Report: Mainstreaming the transition to a net zero economy (2020)

The ability to create this virtuous circle has been greatly enhanced by the recent progress in creating a financial system ready to finance the net-zero transition. COP26 in Glasgow delivered 24 major reforms that are helping transform the information, tools and markets at the heart of finance.

Channelling Paul, this includes measures to ensure financial markets have clear, comparable and decision-useful climate disclosure so they can manage risks and seize opportunities associated with the climate transition. The IFRS Foundation’s new International Sustainability Standards Board, the ISSB, will produce a climate disclosure standard—based on the TCFD—that will ensure investors in over 130 countries have access to the data they need.

In this vein, I welcome the SEC’s consultation on a new US climate disclosure standard17, which is firmly grounded in the demands of an overwhelming number of investors. Drawing on the private sector led TCFD, the Commission’s proposal contains several innovations including requirements to disclose any internal carbon prices, targets and transition plans that companies may have, as well as the line-item impacts of physical and transition climate events on consolidated financial statements. Appropriately, material information is to be disclosed in regular company filings, not tucked away in ESG reports.

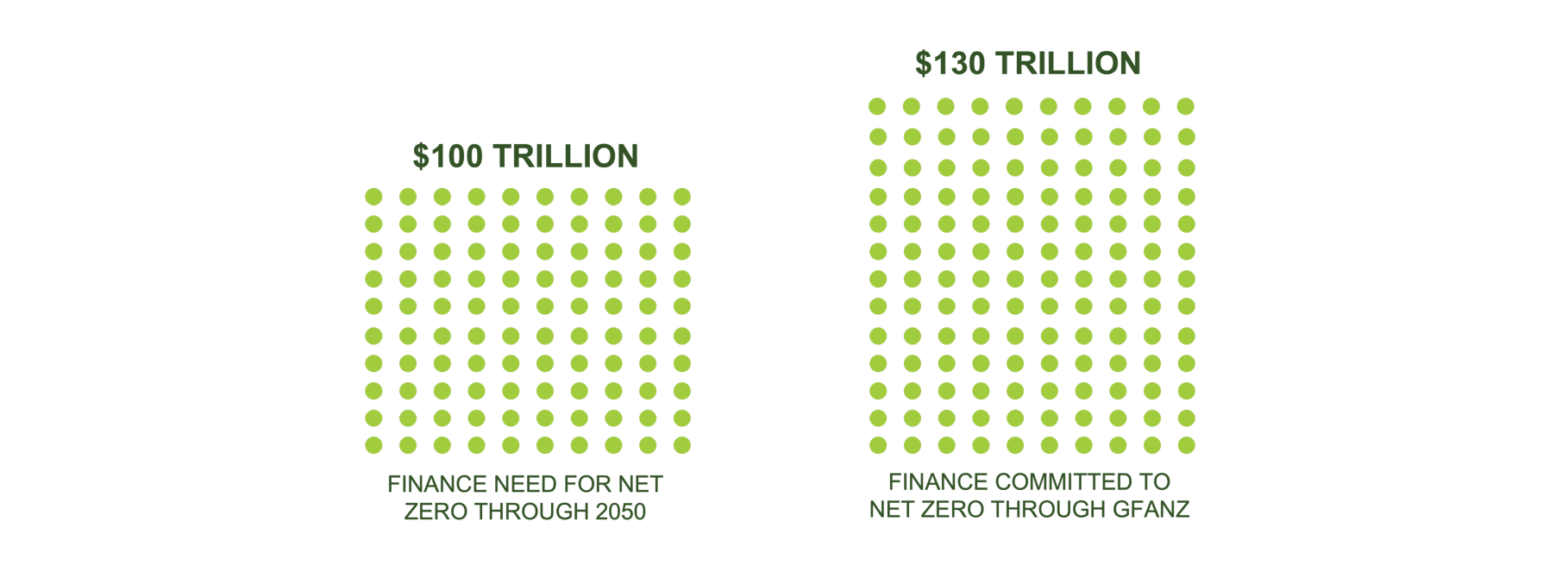

Investor demand for climate disclosure reflects the growing realisation that addressing climate change is one of the greatest commercial opportunities of our time. That’s one reason why, as part of the Glasgow Financial Alliance for Net Zero, over 450 major financial institutions from 45 countries are committing to manage their balance sheets totalling over $130 trillion in line with a 1.5° net-zero transition.18 That’s 40% of all global financial assets (see Figure 16).

Figure 16: 40% of the World’s Financial Assets Are Now Pledged to Net Zero

Source: Glasgow Financial Alliance for Net Zero (GFANZ)

To be clear, the net-zero transition doesn’t mean flipping a green switch or investing only in companies that are already green. Transition means transition. Financial institutions must go to where the emissions are and back companies—including in heavy emitting sectors like steel, cement and transportation—that have credible plans to transform their businesses for a net-zero world. They will also finance traditional energy projects consistent with the climate transition, including helping to phase out stranded assets transparently and responsibly through clear frameworks.

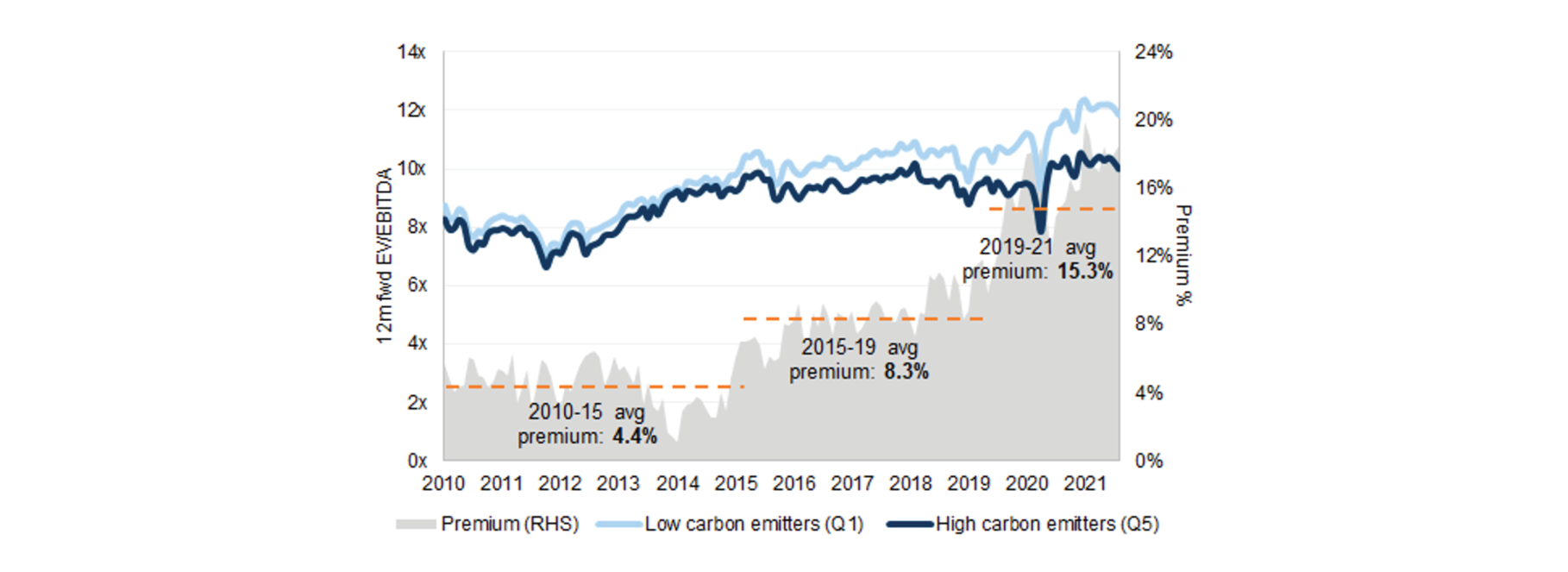

There is increasing evidence that this dynamic is affecting company valuations, starting the virtuous cycle that credible climate policies can reinforce. As one example, lower emitting firms trade at increasing premiums across sectors (see Figure 17).1920

Of course, finance cannot do the job on its own. Finance is an enabler, a catalyst that will speed the transition, but catalysts still need the underlying components, which in this case are the climate policies of countries.

Today’s energy crisis reinforces this imperative. In my judgment, the combination of geo-political considerations, the time scales required to make meaningful changes to energy mixes, the risks of stranded carbon and long-term competitiveness should lead to an acceleration of the clean-energy transition. Clean energy is sustainable, competitive and secure.

For this to become a reality, it is imperative that governments clearly define their energy objectives and allow markets to drive the solutions.

Figure 17: Lower Emitting Companies Across Industries Trade at Premiums

Source: Refinitiv, FactSet, Bloomberg, Goldman Sachs Global Investment Research

V. Conclusion

Although the monetary tightening of the Volcker Fed is firmly in the central banking pantheon, the very human cost of that disinflation should not be forgotten—a brutal recession and millions of unemployed, a “sacrifice ratio” necessitated by the string of errors and timid actions that preceded it

High and volatile inflation at least can be vanquished. It need not be a permanent condition. The same cannot be said of climate change. The world is on course to exhaust our entire carbon budget for a 1.5° world this decade. Caught in the climate version of Paul Krugman’s Timidity Trap21, we are dithering towards climate disaster—a drift that, if allowed to continue, will at best set up a future climate Minsky moment, with policies that cause abrupt and wrenching economic adjustments, strand trillions of dollars in assets, and impair financial, price and potentially geo-political stability.

There is still time to recognise that climate change is macro critical, that climate policy has become the third pillar of macro policy, and that through credible policy coordination we can catalyse enormous private investment that creates jobs, accelerates growth, smooths inflation and promotes energy security.

The degree of climate change is a choice, but the window for making that choice is closing rapidly. Paul Volcker wouldn’t wait.

Disclosures

This commentary and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This commentary discusses broad market, industry or sector trends, or other general economic or market conditions. It is not intended to provide an overview of the terms applicable to any products sponsored by Brookfield Asset Management Inc. and its affiliates (together, "Brookfield").

This commentary contains information and views as of the date indicated and such information and views are subject to change without notice. Certain of the information provided herein has been prepared based on Brookfield's internal research and certain information is based on various assumptions made by Brookfield, any of which may prove to be incorrect. Brookfield may have not verified (and disclaims any obligation to verify) the accuracy or completeness of any information included herein including information that has been provided by third parties and you cannot rely on Brookfield as having verified such information. The information provided herein reflects Brookfield's perspectives and beliefs.

Investors should consult with their advisors prior to making an investment in any fund or program, including a Brookfield-sponsored fund or program.

Endnotes

- I am grateful to Regana Alicka, Zineb Bouzoubaa, Di Chen, Ronan Hodge, Maia Johnson, Simone Kramer and Jen Nemeth for help in the preparation of this lecture, which also benefitted enormously from earlier conversations about the core ideas with Nabeel Abdoula, Jean Boivin, Gavyn Davies, Adam Posen and Jan Vlieghe, as well as from the debate and scrutiny at the Secular Forum of the PIMCO Global Advisory Board. All errors and omissions remain my responsibility.

- Financial Times. ‘Four former Fed chairs call for US carbon tax.’ https://www.ft.com/content/e9fd0472-19de-11e9-9e64-d150b3105d21

- World Meteorological Organisation (2022). https://public.wmo.int/en/media/press-release/2021-one-of-seven-warmest-years-record-wmo-consolidated-data-shows#:~:text=Geneva%2C%2019%20January%202022%20(WMO,by%20the%20World%20Meteorological%20Organization

- Swiss Re Institute (2021). https://www.swissre.com/media/news-releases/nr-20211214-sigma-full-year-2021-preliminary-natcat-loss-estimates

- Swiss Re (2020). https://www.swissre.com/media/news-releases/nr-20201215-sigma-full-year-2020-preliminary-natcat-loss-estimates

- Kirezci, et. al. Projections of global-scale extreme sea levels and resulting episodic coastal flooding over the 21st Century (2020)

- IEA (2021). Net Zero by 2050. https://www.iea.org/reports/net-zero-by-2050

- As Jean Pisani Ferry (2021) calculates, an increase of 2 percentage points (if at global level) would more than reverse the decline in the world investment ratio from 25.7 % in 1980-89 to 24.3 % in 2010-19. Jean Pisani Ferry. August 2021. ‘Climate Policy is Macro-Economic Policy, and the Implications will be Significant.’ Peterson Institute for International Economics Policy Brief.

- Jean Pisani Ferry. August 2021. ‘Climate Policy is Macro-Economic Policy, and the Implications will be Significant.’ Peterson Institute for International Economics Policy Brief. Roughly 36 gigatons of global carbon emissions (2019) would amount to 4.1 percentage points, or 3.7 percentage points above what he estimates as the current average carbon price of $10. In comparison, the 1974 oil shock resulted in the repricing of 19.7 billion barrels of oil from $3.3 to $11.6/barrel; the corresponding shock amounted to 3.6 percentage points of the 1973 global GDP.

- Bartsch, Boivin & Brazier. January 2022. ‘A World Shaped by Supply’, Blackrock Investment Institute. https://www.blackrock.com/corporate/literature/whitepaper/bii-macro-perspectives-january-2022.pdf

- Mark Carney (2017). Globalisation and Inflation. IMF Lecture in Honour of Michel Camdessus. https://www.bankofengland.co.uk/-/media/boe/files/speech/2017/de-globalisation-and-inflation.pdf?la=en&hash=E0C5E30A659BB8F9564F3FA0B3F5C1C1A10F199F

- Mark Carney (2017). ‘Lambda’. Speech at LSE. https://www.bankofengland.co.uk/-/media/boe/files/speech/2017/lambda.pdf?la=en&hash=024E1D5DA7CA7BBD19360E75227E69D805E499CA

- Guerrrieri, et. al. ‘Monetary Policy in Times of Structural Reallocation’ https://www.kansascityfed.org/documents/8322/JH_Guerrieri.pdf

- Note: The corollary is that, in the face of a positive supply shock, the central bank should accommodate some “good disinflation/deflation” for better inter-temporal substitution, a point missed by Greenspan et al. during the productivity boom, with consequences for financial bubbles and instability.

- Net Zero Tracker. https://zerotracker.net/

- G30 Report: Mainstreaming the transition to a net zero economy (2020). https://group30.org/images/uploads/publications/G30_Mainstreaming_the_Transition_to_a_Net-Zero_Economy_2.pdf

- SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors (March 21, 2022). https://www.sec.gov/news/press-release/2022-46

- Glasgow Financial Alliance for Net Zero. www.gfanzero.com

- Goldman Sachs ‘The Dual Action of Capital Markets Transforms the Net Zero Cost Curve’ November 2021. https://wwwqa.goldmansachs.com/insights/pages/gs-research/dual-action-of-capital-markets-transforms-net-zero-cost-curve/the-dual-action-of-capital-markets-transforms-the-net-zero-cost-curve.pdf

- https://esgforinvestors.com

- Krugman, Paul. ‘The Timidity Trap.’ New York Times. 20 March 2014. https://www.nytimes.com/2014/03/21/opinion/krugman-the-timidity-trap.html

Link copied to clipboard!