The movement of money is an essential service supporting the global economy, but it’s struggling to keep up with the pace of technological progress.

To support the 24/7 activity of global commerce, the world’s financial infrastructure requires significant investment to transform legacy frameworks to digitally native, locally adaptive systems.

We believe that the global financial ecosystem is in the midst of a structural transition to tech enablement, with key trends driving rapid changes in the financial infrastructure industry. This has created a $4 trillion private equity opportunity1 to upgrade the essential core businesses that enable the seamless, efficient movement of capital.

Here, we explore these key industry trends, the economic incentive for improving operations and the sectors offering the most value.

What’s Driving This Opportunity?

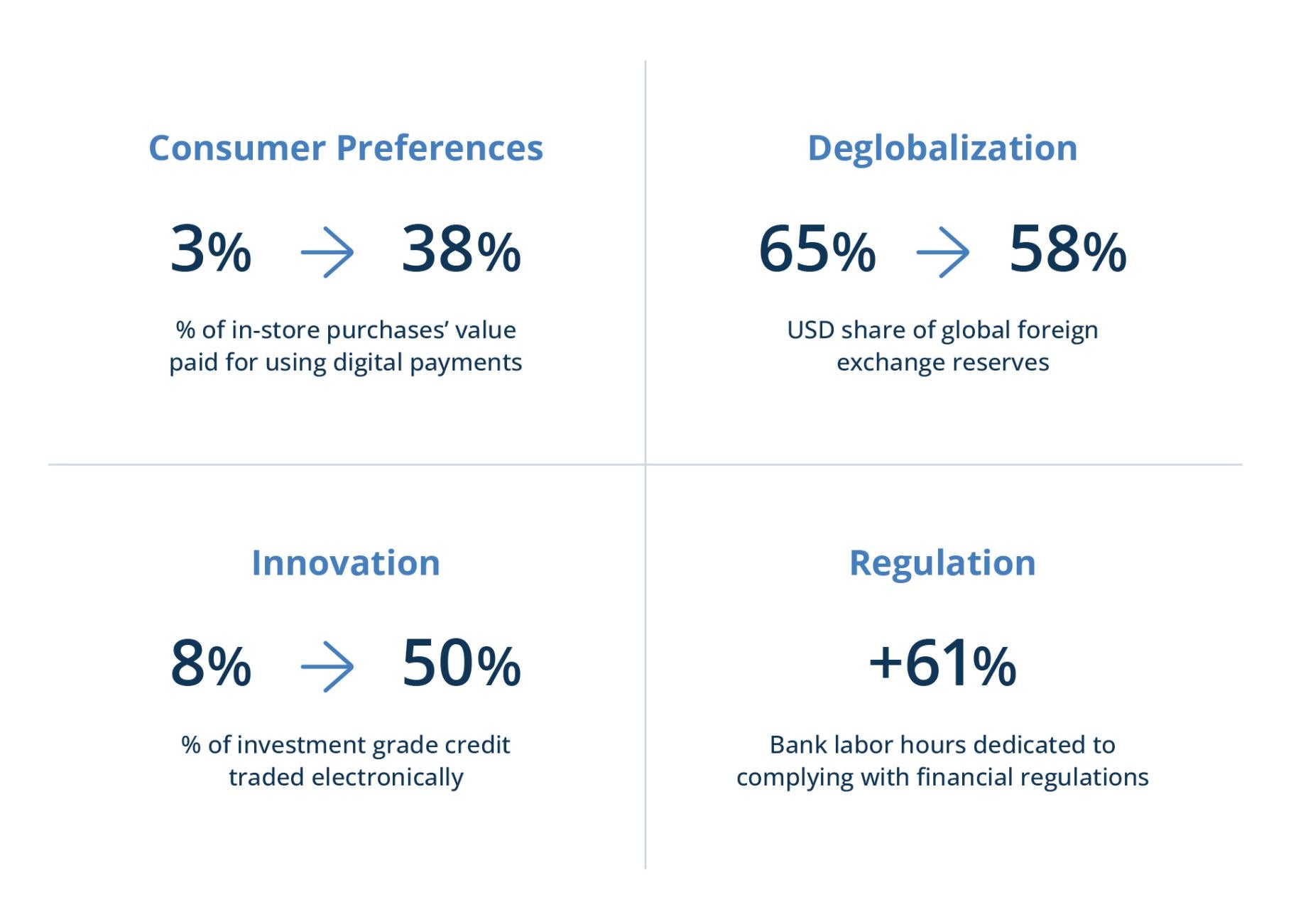

Many of the world’s financial infrastructure assets are held by traditional financial firms operating on decades-old platforms. Yet several transformational trends over the past decade are requiring them to scrutinize those operations and make critical improvements necessary to compete (see Figure 1).

Consumer Preferences: The global consumer population is not only growing but also becoming more sophisticated and demanding. Broader access to products and services is requiring businesses to adopt an unrelenting focus on improving the user experience, including security.

Deglobalization: Geopolitical forces are driving the world away from globalization and toward localization of products of services. This trend is forcing companies of all sizes to rethink their supply chains and routes to market, leading to greater industry fragmentation such as regional payment systems.

Innovation: New business lines are emerging as companies seek to drive technological advances and build highly scalable platforms. For example, new forms of payments such as digital wallets are gaining broad acceptance and challenging the traditional card payment ecosystem. The need to match these capabilities will increase capital requirements for traditional financial companies.

Regulation: Compliance requirements for financial service companies continue to become more sophisticated, driving growth in regulatory technology solutions that drive efficiency and reduce costs. For example, over 70% of countries worldwide have adopted data protection and privacy legislation,2 raising the level of compliance and costs required in jurisdictions around the world. Financial services companies will need to spend more to minimize security risks, increase data sovereignty and reduce their exposure to data breaches and regulatory challenges.

Figure 1: Four Key Trends Are Revolutionizing the Movement of Money

Source: See endnote 3.

Financial Infrastructure Must Catch Up to Global Commerce

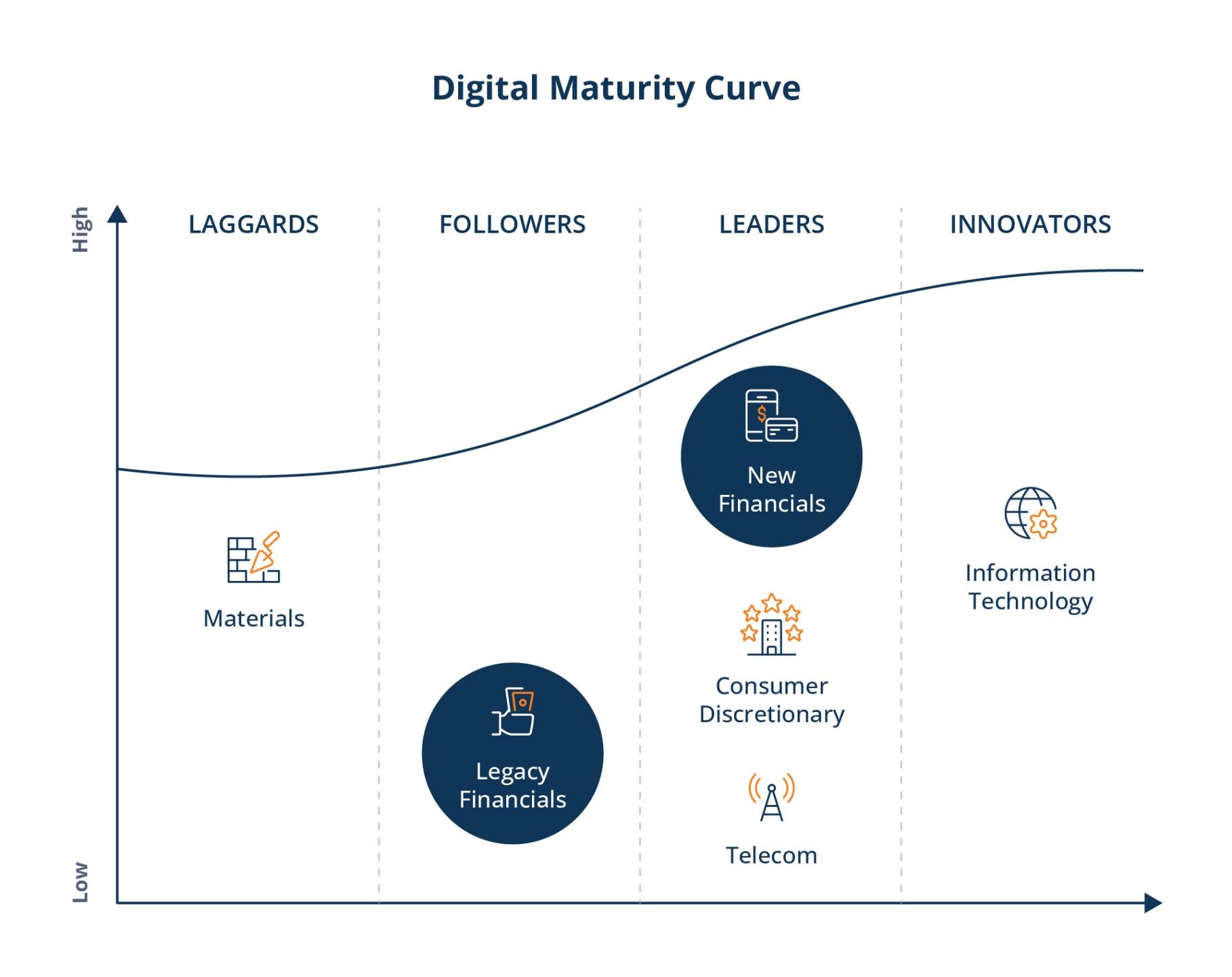

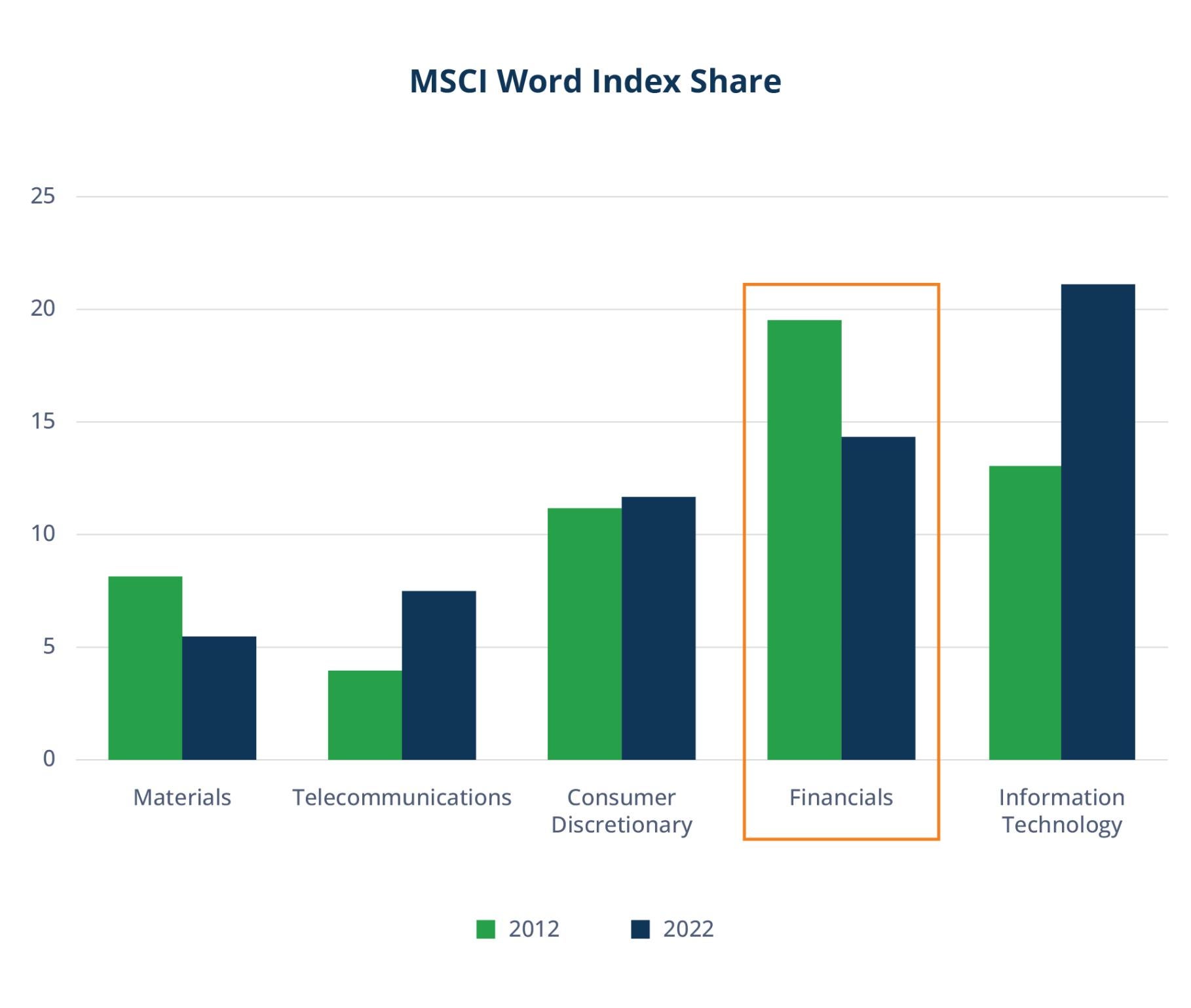

Technology advancements have penetrated different asset classes at varying speeds, with early adopters gaining the most market share. While sectors like IT have grown as a share of the global economy, the financial services industry has lagged others in the push toward modernization over the past 15 years (see Figures 2 and 3).

Legacy financial companies rank low on the digital maturity curve—a framework that helps businesses assess their current level of digital transformation and chart a path for growth. Yet many are high-quality businesses that simply lack the capital and expertise to upgrade their analog systems to new-age digital operations. This environment is creating opportunities for experienced private equity managers to provide the large-scale funding and operational expertise that many of these businesses desperately need to improve their financial infrastructure.

Figure 2: Industries Slow to Adopt Technology …

Source: Moneycontrol.com.

Figure 3: … Have Lost Share in the Global Economy

Sources: MSCI, “The Regional Breakdown of Market Sectors Over Time.”

Where Are the Opportunities?

In our view, four sectors offer more than 80% of the $4 trillion financial infrastructure opportunity, with many of the businesses in these sectors misunderstood by investors or underutilized by corporate owners. Rising consumer expectations and demand coincide with rising operating costs that many financial infrastructure companies cannot absorb:

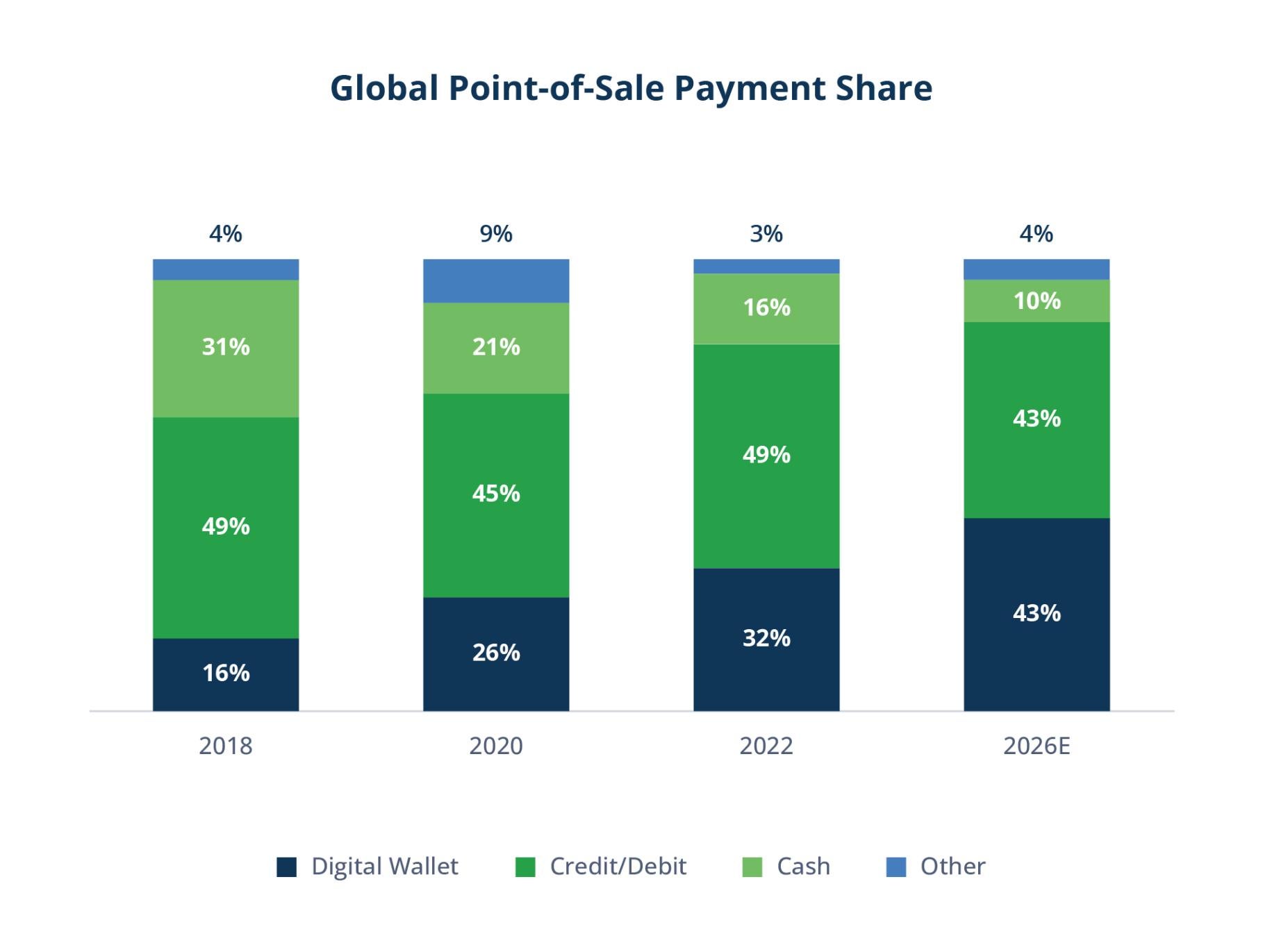

In the payments sector, for example, the pandemic accelerated a shift among consumers away from cash and toward digital payments. That shift continues, as cash usage declined by nearly 4 percentage points globally in 2022, according to McKinsey.4 And as consumers become more accustomed to digital alternatives, their expectations grow. From cash to checks to credit cards to digital wallets and biometric payments like fingerprint scanning or facial recognition, consumers are less willing to fumble for their wallets when it’s time to pay up. Although payment options like these have not yet overtaken credit cards, the world is increasingly becoming digital-first (see Figure 4). Digital wallets, for example, are expected to increase to over 40% of the global point-of-sale payment share.5

Figure 4: Many More Ways to Pay

Source: WorldPay, “The Global Payments Report,” 2018, 2021 and 2023 editions.

And it’s not just payments. Challenges like these are being confronted in almost every facet of the $28 trillion financial services economy. For example:

In the capital markets sector, volatility is rising from rapidly evolving macroeconomics, wealth dynamics, market participation and consumer preferences. With data and analytics investments driving growth, companies need to upgrade their infrastructure to facilitate the flow of capital from investors to equity issuers and secondary exchanges.

In the banking technology sector, critical investments in the customer experience are required to meet banking service expectations. Financial institutions with limited in-house capabilities, such as credit unions and community banks, are seeking scalable and cloud-based software that can more seamlessly facilitate everything from opening a new account to applying for a loan. This heavily regulated sector requires updates for all relevant regulations affecting its products and services.

In the wealth sector, the need to give consumers choice and eliminate paper-based processes is enabling service platforms that act as the pipeline for third-party funds to be distributed through legacy wealth management channels. Companies in this sector are increasingly using outsourced third-party platforms or software to satisfy increasingly complex client needs. Tailwinds include underlying growth in global household wealth, with an increasing proportion of these assets being invested in independently advised channels.

Looking Ahead

These trends mean that many financial services companies will have to fundamentally change their business models so they can develop digital solutions to meet their customers’ needs and operate in a rapidly evolving global economy. That will require heavy investment in areas that, for many financial services conglomerates and banks, are not part of their core businesses—despite being foundational to the global economy. We are already seeing many of these assets moving off these companies’ balance sheets, creating attractive opportunities in this “invisible” infrastructure sector.

This commentary and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This commentary discusses broad market, industry or sector trends, or other general economic or market conditions. It is not intended to provide an overview of the terms applicable to any products sponsored by Brookfield Asset Management Inc. and its affiliates (together, "Brookfield").

This commentary contains information and views as of the date indicated and such information and views are subject to change without notice. Certain of the information provided herein has been prepared based on Brookfield's internal research and certain information is based on various assumptions made by Brookfield, any of which may prove to be incorrect. Brookfield may have not verified (and disclaims any obligation to verify) the accuracy or completeness of any information included herein including information that has been provided by third parties and you cannot rely on Brookfield as having verified such information. The information provided herein reflects Brookfield's perspectives and beliefs.

Investors should consult with their advisors prior to making an investment in any fund or program, including a Brookfield-sponsored fund or program.