Letter to Shareholders

Contents

Bruce Flatt

Chief Executive Officer

01Overview (As of February 13th, 2020)

Stock market performance was very strong in 2019. Our shares in particular generated an overall return of 50% during the year. While this was due in part to the overall market performance, it was also the result of our strong operating results. Fundraising for alternative investments, which are becoming more mainstream every day, remains strong. Post year end, we closed our latest flagship fund of $20 billion for Infrastructure. We also continue to fundraise for our perpetual core-plus funds which today near $8 billion in total size. With interest rates continuing to be very low, these funds should attract greater amounts of capital as the strategies mature.

We invested over $30 billion during 2019 and sold $13 billion of investments. Our investment strategies are focused on a few themes: the global build-out of renewables, data infrastructure, high-quality property developments, and global businesses where our operating expertise helps generate returns greater than might otherwise be expected. With our franchise continuing to globalize and the scale of our capital growing, we see no reason 2020 won’t be as good a year operationally as 2019.

Much attention is being paid these days to sustainability and carbon footprint. As many of you know, we have been very active in this area without much fanfare. The sheer scale of our renewables business and its avoided emissions eclipse our estimates of emissions across all our other businesses. On this basis, we believe Brookfield’s overall carbon profile today is very low, if not neutral or possibly even negative. We intend to further enhance that profile as we build out our vast development portfolio of renewables.

We have decided to split our shares again on a 3-for-2 basis, and in conjunction with this, increase the dividend by approximately 12% — which will therefore be 18 cents per share at the end of March, and 12 cents per share on a quarterly basis, post-split. While splitting the shares has no effect on the value of the company, it costs us virtually nothing to do, and it has been our practice to do this, as it keeps the share price within a reasonable range for investors.

02Stock Performance

While we manage our underlying business for the long term, we realize that you are also interested in our stock performance. Its 50% increase in 2019 was an anomaly; at the same time, the previous year the share price was down, which we also viewed as an anomaly. We estimate that we earned approximately 20% annual returns on our intrinsic value over the two years. As a result, over the two years combined, our stock had a return that was about the same as what we generated in the business.

Most importantly, our view of the intrinsic value of the business continues to increase. This is because most of our businesses performed well, and because we raised significant capital to deploy into new opportunities. This should enable us to deliver favorable results well into the future.

As an indication of returns that can be generated for investors, below is our latest tabulation of annualized compound investment returns over the past 25 years. For reference, $1,000 invested 25 years ago in Brookfield Asset Management is today worth just over $62,000.

03Market Environment

The global economy is still very constructive, in spite of the fact that we are in the later stages of a bull market. With interest rates very low around the world, we think this cycle could last longer than anyone expected. Regardless, we are ensuring that we are not complacent at this point in the cycle.

Developed economy markets show no signs of stress. However, the fact that equity markets have been very strong for the last year in itself is worrisome. The corporate credit markets also are performing well, but we believe this is where the great value will be found in the next downturn. We are positioning ourselves to capitalize on this — both through our Brookfield funds, and through Oaktree.

The United States, Canada, and Australia have strong economies, but assets are more fairly priced. As a result, we continue to be selective with opportunities, looking for transactions in out-of-favor sectors and focusing on opportunities that play to our operating strengths.

Europe is slower but still resilient. Opportunity lies in the fact that 60% of the capital invested in an acquisition can be borrowed at virtually no cost. The United Kingdom seems to have pushed past its Brexit crisis, which should be positive for businesses making long-term commitments.

Companies in India and China are under stress (the latter compounded with the recent virus issues) — banks in India are dealing with non-performing loans, and in China they are pushing borrowers to sell assets. This has led to significant investment opportunities that we think will continue for the foreseeable future.

Brazil looks to be back on track to continued recovery, with interest rates now under 5%, down from close to 15% in its most recent financial crisis. As a result, fixed income and equity investors have had excellent returns, and private assets have followed suit.

04A Summary of 2019

Total assets under management are now $545 billion (including Oaktree), as we continue to raise and deploy additional capital across our businesses.

Asset Management Activities

We now own 61% of Oaktree, with the balance continuing to be owned by the Oaktree partners. Joining with this premier credit franchise deepens the capabilities we offer our clients, positions us even better across market cycles, and expands our breadth as one of the world’s largest alternative asset managers. While Oaktree will continue to operate as a standalone business, the world-class management team and credit expertise they bring have already had a positive impact on our business, and the benefits should continue to compound over time.

Organic growth within our existing asset management business was very strong. In January 2019, we closed our latest flagship real estate fund at $15 billion, an increase of over 65% from its predecessor fund. We also held the final close of our latest flagship private equity fund at $9 billion in October, more than double the size of its previous vintage. Finally, we recently held the final close of our latest flagship infrastructure fund at $20 billion, making it one of the largest global infrastructure funds ever raised.

Together, this round of flagship fundraising raised over $50 billion, including co-investment capital, and is already approximately 45% deployed. Our flagship Oaktree distressed debt fund is also over 40% deployed, and all of the capital committed to it became fee earning as of January 1, 2020. As a result, it will begin to fully contribute to results this year. Our focus for 2020 will be on growing our other strategies, while also deploying the latest round of flagship capital. If successful, we anticipate that we will be back in the markets with our next launch of flagship funds late this year or in 2021.

Fundraising for our specialized strategies had strong momentum in 2019. We raised $3 billion of capital within our perpetual private fund strategies across our super-core infrastructure and core and mezzanine real estate funds. We also recently launched the second vintage of our private infrastructure debt fund in the fourth quarter.

With respect to fund distribution, our high net wealth channel is growing steadily and today accounts for approximately 10% of funds raised on an annual basis, making a meaningful contribution to our latest round of flagship funds. While the geographical split of capital raised across all channels has remained largely consistent with the prior year, the number of LPs and total dollar value of capital raised from target geographies, including Asia and Europe, is growing.

Growth in the asset management franchise drove fee-related earnings prior to performance fees to $1.2 billion, a 41% increase from the prior year. We also realized a greater level of carried interest in 2019. We recorded in income approximately $600 million of carried interest during the year, reflecting the completion of a number of asset sales within our earlier vintage flagship private funds, which crystalized investment gains and the associated carried interest. We expect continued realizations in 2020, as we progress planned asset dispositions in each of our flagship fund strategies.

Operating Activities

Despite the record levels of capital flowing to alternative asset managers in 2019, we found many opportunities to deploy capital for value. We invested over $30 billion of capital across our business groups by leveraging our key strengths of access to diverse pools of capital, global scale and operating expertise. We also realized $13 billion of proceeds from the sale of mature assets.

Our real estate operations made many investments globally, including an investment in the hospitality sector in India, and one in the retail sector in Dubai. We also acquired a business in the senior housing and assisted living sector in Australia. We progressed on our redevelopment and densification strategy within our core retail portfolio, and completed over 4 million square feet of office developments in New York and London. Average rents across our office portfolio increased 2% since this time last year. With significant developments and acquisitions coming online in the near term, we expect growth to continue in 2020.

Our renewable power operations continued to grow in scale and reach. We partnered to acquire a 50% interest in one of the world’s largest solar developers. We doubled both the size of our Asian operations, and our distributed generation businesses. We also made a sizable investment in a utility company, with an option to acquire an interest in their hydro portfolio. At the same time, we progressed our capital recycling program, selling wind portfolios in Europe, as well as the majority of our South African solar and wind assets. From a green financing perspective, we issued in aggregate $1 billion of green financings, including the largest-ever corporate green bond in Canada. Lastly, since year end we announced the combination of Brookfield Renewable and TerraForm Power in an all-stock deal.

Our infrastructure operations continued to deliver strong results, increasing normalized FFO by 12% from the prior year. Results were driven by organic growth and the acquisition of a number of businesses, including natural gas pipelines in North America and India, and data infrastructure businesses in India, South America and New Zealand. At the end of December, we also closed on the acquisition of one of the largest short-haul rail operators in North America, a cell-tower business in the U.K. and a portfolio of pipeline assets. These latest acquisitions will begin to contribute FFO in the first quarter of 2020.

Our private equity operations continued to grow in scale, with the acquisition of a number of high-quality businesses. Most notably, we acquired a leading global supplier of advanced automotive batteries and the second-largest private healthcare provider in Australia. We also acquired a controlling interest in a residential mortgage insurer in Canada and announced an investment in a leading provider of work access solutions to industrial and commercial facilities. On the disposition front, we sold our global facilities management business, our executive relocation business, a palladium mining company, and a cold storage business, each for very strong returns.

Our credit operations delivered good results during the year, especially in the Oaktree franchise. Our Brookfield infrastructure and real estate debt funds also continued to perform well, with significant capital deployment. The economic outlook currently warrants a disciplined approach, with a measured pace of lending across the debt funds. We continue to deploy capital the same way we always have — with an emphasis on fundamental analysis and downside protection of capital.

Overall, our share of the underlying funds from operations from our invested capital increased 9% over 2018, to $1.7 billion before disposition gains. The growth in FFO from our invested capital, combined with the earnings from our asset management franchise, generated $2.6 billion of free cash flow to BAM in 2019. As our free cash flow has more than doubled over the past five years, and we expect it to do so again over the next five years, we continue to evaluate the best use for this cash flow — whether that be re-investment within our business; seeding new strategies; opportunistic investments such as the Oaktree acquisition; or returning value to shareholders through other means such as share repurchases or increased dividends. Rest assured we think all the time about the best use for your capital.

05The Advantage of Asset-Level Non-Recourse Financing

Like many other investors, we utilize debt to optimize our capital structure and fund our business. However, unlike many others, as both an asset manager and investor, how we report the debt in our financial statements is different from most other businesses. For that reason, we think it important to devote a few paragraphs to this.

We take a bottom-up approach to financing the investments we manage. That means that the vast majority of our debt is at the individual asset (or portfolio company) level. Each loan has recourse to only the specific asset that it finances — and importantly, gives lenders no recourse to BAM or our listed partnerships. As a result, the risk of anything going wrong with any financing is limited solely to the equity invested in that particular asset. No single loan can ever create a forced liquidity event for the broader franchise or even parts of the franchise.

Despite the foregoing, we structure our financings to stand the test of time and withstand adverse circumstances, and we have a strong track record that proves this out: we fared well in 2008/2009, which demonstrated the strength of our prudent approach to financing. We take pride in being one of the highest-quality borrowers in the capital markets.

As a Canadian firm, international accounting principles require us to consolidate many of these investments, including their borrowings, in our consolidated financial statements for reporting purposes — even though our proportionate economic ownership of the investment is in most cases well below 50%. The requirement to consolidate is due to the combination of (1) the control over these activities that we exert; (2) compensation we receive as the manager; and (3) our economic interest in the assets. This results in the appearance that Brookfield has more debt outstanding than it actually has.

The debt that is most relevant to Brookfield shareholders is the debt issued directly by the Corporation. This debt currently totals $7 billion — a significant sum to be sure, but it is all very long-term in nature and modest relative to Brookfield’s $72 billion capitalization of common and preferred equity.

In a similar vein, each of our listed partnerships utilizes modest amounts of corporate debt to manage its capital resources for its unitholders. We manage these entities to have investment grade characteristics which enables them to finance their activities on a standalone basis, without any recourse to BAM. Currently our four listed partnerships combined have $6 billion of corporate debt compared to an aggregate equity capitalization of $69 billion.

With this context in mind, we encourage you to look at the disclosures in our MD&A that present the corporate, listed partnership and asset level debt in a way that is more consistent with our approach to leverage, as described above.

06The United Kingdom is Stronger Than it Seems

Our view is that the long-term effects of Brexit on the City of London will be negligible. Despite that, we were pleased that the Conservative Government in the U.K. received a clear mandate to leave the E.U., and can now proceed with the logistics of the process. While years ago we would not have wished for this, the only scenario that was truly negative for the U.K. was the ongoing indecision.

Overall, our businesses across the U.K. — which include office buildings, ports, utility businesses and student housing, among others — have performed well to date despite the headlines and politics. A great example of this is our 100 Bishopsgate development. We acquired 50% of the land at 100 Bishopsgate in 2010, then acquired the remaining interests from the partner in 2014, and planned a 950,000-square foot office tower with associated retail. We began construction in 2015, and our total acquisition and construction costs were approximately £850 million.

In June 2016, when the Brexit vote occurred, we were 50% complete on construction, with 38% of the space leased to tenants. Since Brexit (about 3½ years), we have completed the construction on budget and leased nearly all of the balance of the tower on a long-term basis. More importantly, that additional space was leased at or above the rental rate levels we expected when we started.

As a result, we will soon have annual cash flows from 100 Bishopsgate, net of costs, of £70 million. We recently refinanced the property with a loan for £875 million, essentially our cost. The interest rate on the recourse-only mortgage is 3%, or £27 million annually. We now have no remaining equity investment cost, and we enjoy cash flows net of interest of £40 million annually. Capitalization rates for this type of property would today be between 3% and 4%. At the low end of this range, the value created is £900 million over our cost. At the high end, it is £1.5 billion of profit over our cost. This was a good outcome under any circumstance, but given the backdrop of Brexit, is exceptional. Most importantly, this gives an indication of what is occurring in the real economy in the United Kingdom.

07The Sun is Shining Even Brighter

We have been invested in renewable power in a significant way for 30 years, as a result of our original ownership of hydro facilities associated with industrial facilities we owned. We expanded the operations into wind, and more recently into solar, as technological advances and scale manufacturing enabled the costs of production to decrease below those of traditional forms of electricity in many parts of the world.

While the renewables sector has had its share of turmoil over the years as it matured, our private clients and listed partnership investors have all done extremely well financially, as we continued to adhere to our investment principles. As an indicator of these returns, our stock exchange-listed partnership, Brookfield Renewable Partners (BEP), has generated a compound annual return of 18% over the past 20 years.

Today we are a leading renewables investor globally with $50 billion of solar, wind and hydro facilities in 17 countries. As the global energy supply continues a slow shift to renewables, we are ideally positioned to capitalize on opportunities in the renewable market.

Since we wrote about this two years ago, the transformation has increased, and today everyone seems to be interested. We think we are still in the early stages of this transformation, and it will require very substantial capital investment over multiple decades.

Renewables still account for less than 30% of the global electricity production, of which wind and solar account for less than 25% of the current renewables in place. Accordingly, even if the world maintains its current $300-$400 billion of annual investment into renewables, the level of penetration will remain modest for years.

08Retail is Evolving

There are many views around the world about how the retail landscape will shake out. Last year we took private our retail mall property business which had been listed in the public markets. In the process we acquired 125 incredible parcels of land in major cities across the U.S. We plan on developing these into many tens of thousands of residential apartments and condominiums, office properties, hotels, warehouses and self-storage locations. With these land parcels, we acquired a premier retail business that generates over $2 billion of EBITDA.

While this is broadly seen as a contrarian investment, our views are very simple. First, the internet and physical retail will ultimately merge into one delivery network to customers, and as a result, great retail will get even better. Second, retail real estate presents redevelopment opportunities — and with our strong development capabilities, we will be able to add income to these sites for decades to come.

It is very important to distinguish between the different types of retail. Our view is that good retail, focused on ‘experiences,’ will only get better — real estate is always about location and what can be done with that location. On the other hand, average-to-poor retail will continue to struggle. Our retail mall portfolio is one of the highest quality portfolios in America — and as a result, we are 96% leased on a long-term basis. Furthermore, retailers are consolidating stores into the best malls. In time, like almost all industries, consolidation will end and the survivors will be stronger for it.

Part of our confidence comes from the fact that we are dealing with a growing number of retail brands that started life online but are now opening stores at a record pace. Even Amazon is opening stores to attract customers. This is because the most inexpensive way to attract customers once sales achieve any scale is to open stores. In the last year, over one-third of our new leasing activity was completed with emerging retailers. Among these growing brands, 60% are retailers that started with online operations only — sometimes referred to as ‘clicks to bricks.’ As this plays out, good retail will only get stronger.

Lastly, these retail centers sit on 100+ acre land parcels which happen to be located in the most densely populated and wealthiest cities in the U.S. We are only starting to redevelop the land around them with offices, apartments, condominiums, hotels and other property uses. The next 50 years will offer us significant upside in what we view as one of the highest-quality land redevelopment portfolios ever assembled in the United States.

09Our Partnership Approach

As many of you know, our senior management team has operated as a partnership for over 25 years. This approach has, first and foremost, provided important stability and continuity to Brookfield over the years — and we believe is one of the reasons we have been able to generate compound returns of approximately 20% for ALL shareholders over that period. We took great care in structuring the partnership, and it has been a driving force in how we run the business — and, in turn, has had a very positive impact on our culture. We have always managed Brookfield in a non-hierarchical and collaborative way, working to make the whole greater than the sum of the parts by operating as a team, sharing credit, methodically planning and managing succession, and promoting from within wherever possible.

Brookfield is a public corporation that has many important benefits for shareholders including stock market liquidity and high levels of governance standards and transparency. At the same time, the capital structure, which was established in 1995, facilitates maintaining our partnership approach and enables long-term decision-making. Through this capital structure, a group of current and former executives of Brookfield have joint control, and are key stewards of the company. This control takes the form of ownership of the Class B shares of Brookfield, which entitle the partnership to elect half the Board of Directors. Owners of the Class A shares elect the other half of the Directors. Our partnership considers the Class B shares to be essentially held ‘in trust’ for the next generation of partners, which makes our focus on teamwork and succession even more important.

The partners collectively also own or have beneficial interests in approximately 20% of the Class A shares of Brookfield. This substantial economic ownership interest, built up over the last 50 years, today amounts to an investment in Brookfield of over $10 billion. It ensures that our interests are strongly aligned with yours. We are also always working through the planning for the next generation in order to ensure continued and seamless succession in the partnership.

In summary, we are focused on ensuring that control of the company will always rest with partners whose interests are fully aligned with all Brookfield shareholders and investors. They are the leaders of our businesses and have very meaningful ownership interests in the firm. We think this has been — and will continue to be — critical to our business success. It provides important continuity and stability, and the meaningful equity ownership in turn fosters a long-term commitment to our business by our senior executives, and management of Brookfield.

10Closing

We remain committed to being a world-class alternative asset manager, and to investing capital for you and our investment partners in high-quality assets that earn solid cash returns on equity, while emphasizing downside protection for the capital employed. The primary objective of the company continues to be generating increased cash flows on a per-share basis and as a result, higher intrinsic value per share over the longer term.

On a more personal note, Brian Lawson who has been our CFO since 2002, will transition out of that role to become a Vice Chair, working a bit less but still watching over risk management for us. Brian has made a significant contribution to our business over many years, so on behalf of all of us here at Brookfield, I want to thank him for his years of dedication. Nick Goodman, who has been with Brookfield for nearly a decade, will replace Brian as Brookfield’s CFO. Nick, currently Treasurer and Head of Capital Markets, has broad experience across our businesses and regions and has been working directly with Brian and me for a number of years. We look forward to introducing Nick to you.

Please do not hesitate to contact any of us should you have suggestions, questions, comments, or ideas you wish to share.

Sincerely,

Bruce Flatt

Chief Executive Officer

Note: In addition to the disclosures set forth in the cautionary statements included elsewhere in this Report, there are other important disclosures that must be read in conjunction with, and that have been incorporated in, this letter as posted on our website at https://bam.brookfield.com/en/reports-and-filings.

In light of the extreme market volatility triggered by COVID-19 in March, 2020, Brookfield Asset Management published an Update for Brookfield Shareholders on March 23, 2020 — included in this year’s Annual Report:

Update for Brookfield Shareholders

As of March 23, 2020

Dear Shareholders,

Given all the market volatility of the last few weeks, we thought it would be helpful to provide an update on where we stand as a company. No one is immune to the issues we are all dealing with, but as you know from our letters over the years, we have been expecting a recession and market washout for some time. Nobody could have predicted that the coronavirus would be the cause, but the markets sure turned over the last month.

As to our positioning and readiness for this, we believe we are in very good shape. We think it is important for you to know a few points:

• We have approximately $12 billion of bank lines in BAM and our four listed affiliates, all of which are very long-term, and importantly are all virtually 100% undrawn with global financial partners who we trust.

• We have approximately $5 billion of financial and non-core assets that can be liquidated with relative ease (even in today’s markets) should we so choose, to fund strategic investments or take care of issues. Many of these are hedged with index hedges so even if markets are down, this should offset marks that may come about due to the environment.

• We have only $7 billion of corporate debt (against an equity market cap of $40 to $60 billion — depending on the day) and none of that debt is coming due for many years. Similarly, in our private funds and listed affiliates, we have very little debt coming due over the next few years. To the extent that we have debt due, they are financings and mortgages secured by individual assets (which confines any impact to the asset). However, even in 2008/09 we were able to roll those over.

• We have no ‘hung purchases’. In fact, it’s the opposite — one way or another, every contested deal we tried to do over the past five months, we lost. We remained disciplined, which meant that we did not buy a number of businesses as their price rose. In hindsight, this was good.

• We just finished raising our latest funds and co-investments, totaling over $50 billion. These are only 40% invested, so we have a lot of capital to put to work in this environment. We also have the support of many leading sovereign and institutional investors in the world to augment these resources.

• We partnered with Oaktree last year in anticipation of the debt markets unwinding. Now it’s taking place. The team at Oaktree is accelerating the pace of deployment of their current distressed debt fund and preparing to launch their next fund, which we think could significantly exceed the size of their last. If this turns out to be the case, the addition of this business to ours will be very additive for us and our clients.

• Most of our businesses are very resilient, and we therefore don’t foresee major issues. Of course, with people staying home, business is slowing everywhere. In our operations, for example, our malls will be operating at a significantly reduced rate for a while (but this is a second derivative exposure as we collect rent, not run the stores, and our financing structures are in good shape), and fewer ships will travel to our ports. The bottom line is that while there are certain to be issues across our portfolio, our businesses are diversified, our financing structures are time-tested, and our resources significant to deal with this.

• Much of what we own around the world is critical infrastructure — across our property, infrastructure, renewable power and industrial businesses. We are working with governments and our employees to ensure that these facilities remain operational through this period. While many are at home now, people and companies still need corporate premises, infrastructure, power, broadband, utilities and many other critical services that form the backbone of the global economy, and that Brookfield’s businesses provide. Our teams are doing their best to ensure uninterrupted delivery of these services for our customers, while operating under difficult circumstances.

As to what we do now, here is how we are approaching this market volatility and uncertainty:

• Most importantly, we are staying calm and ensuring our people are safe. For us, compared to the direct hit we took on 9/11, this uncertainty and volatility feels manageable. In 2008, with the banking system failing, real asset owners didn’t know if many lenders were going to exist in the future. Today, the banking system is in far better shape. It never feels very good to have this degree of chaos, but this will pass.

• We are being vigilant and will continue to be disciplined. We will maintain capital for our worst-case scenarios. This is always very important, but even more so now.

• We have switched our focus for investments to the listed stock markets, and through our Oaktree franchise, the traded debt market. There are some stocks and debt starting to trade at a large discount to intrinsic value and we are focused on these. We are also starting to receive calls from companies in need of capital, and we look forward to being helpful to companies in need, where we can.

• Our shares have sold off along with everything else. We have been acquiring, and will continue to acquire our own shares for value when it makes sense — and in time, we are certain they will recover.

• Interest rates are now 100 basis points lower than they were a month ago. The value of many real assets is therefore higher, and our clients’ need for our offerings even greater. In time, this will all flow through to our assets and the valuations of our business.

Finally, a reminder regarding investing in times like these: the underlying value of a business that trades in the public market does not change on an hourly basis. Despite the fluctuations, you own a part of an actual business, not a piece of paper or electronic symbol that adjusts on a minute-by-minute basis.

Acknowledging that the value of some businesses has changed, at least in the short term (airlines being the most extreme example at the moment), the long-term value of many companies — i.e., the discounted stream of cash flows based on an estimate of growth and durability into the future – has not changed substantially over the past few months. The proviso is that a company must be able to pay its liabilities when due (stay solvent), which of course will be an issue for numerous companies in the absence of government assistance. Our focus has always been on structuring our affairs to ensure we can survive all environments, and we are confident we are in this position today.

Most of our cash flow streams are of very long duration with long-term property leases, long-term power sale contracts, and long-term regulated utility rates that provide durable business revenues with strong counterparties. As a result, the change in value of our businesses in the stock market over a few months has very little to do with the underlying businesses that you, as a shareholder, own. Please remember that you each own a portion of the investment management fees our business generates, as well as a portion of each of the durable businesses and assets we own

It would be less distracting if we all owned this business together privately. That way you could read our materials, look at how each of our businesses is doing, observe the cash flows projected for many years, and not worry about how the stock market, with its short-term focus, values this information. We publish our views of how we value this business, and we encourage you to focus on these values over time (adjusted upward or downward as you see fit) and not on the stock price when volatility is at an extreme. In fact, the main reason to consider the stock price at moments like these is that it allows you to acquire a portion of our business at a large discount from its real value.

It is very easy to invest in the markets when times are good, but it is in times of market decline that following the tenets of value investing matters most. We encourage you to follow them. We know this is a very stressful time for everyone. Please know that we are watching out for your capital.

Be safe and please wash your hands,

Bruce Flatt

Chief Executive Officer

March 23, 2020

Brookfield at a Glance

01Our Business

We are a leading global alternative asset manager with over $540 billion of assets under management including $290 billion in fee-bearing capital. We raise private and public capital from the world’s largest institutional investors, sovereign wealth funds and individuals, with a focus on generating attractive investment returns that will allow our investors and their stakeholders to meet their goals and protect their financial future.

Investment focus – Real estate, infrastructure, renewable power, private equity and credit

Diverse product offering – Core, value-add, opportunistic and credit strategies in both closed-end and perpetual vehicles

Focused investment strategies – We invest where we have a competitive advantage, such as our strong capabilities as an owner-operator, our large scale capital and our global reach

Disciplined financing approach – Debt is carefully employed to enhance returns while preserving capital throughout business cycles

In addition to our asset management activities outlined above, we invest significant capital from our balance sheet in our managed entities alongside our investors as well as in other direct investments. This is intended to generate attractive financial returns and cash flows, support the growth of our asset management activities and create an important alignment of interests with our investors. We refer to this as our Invested Capital and it totals approximately $47 billion.

Asset Management

We provide a wide range of investment products, primarily focused on real estate, renewable power, infrastructure, private equity and credit

Real Estate

Office, retail, industrial, multifamily, hospitality and other properties

Infrastructure

Utilities, transport, energy, data infrastructure and sustainable resource assets

Renewable Power

Hydroelectric, wind, solar and other power generating facilities

Private Equity

Business services, infrastructure services and industrials

Credit

High yield bonds, corporate debt, distressed debt and convertible securities

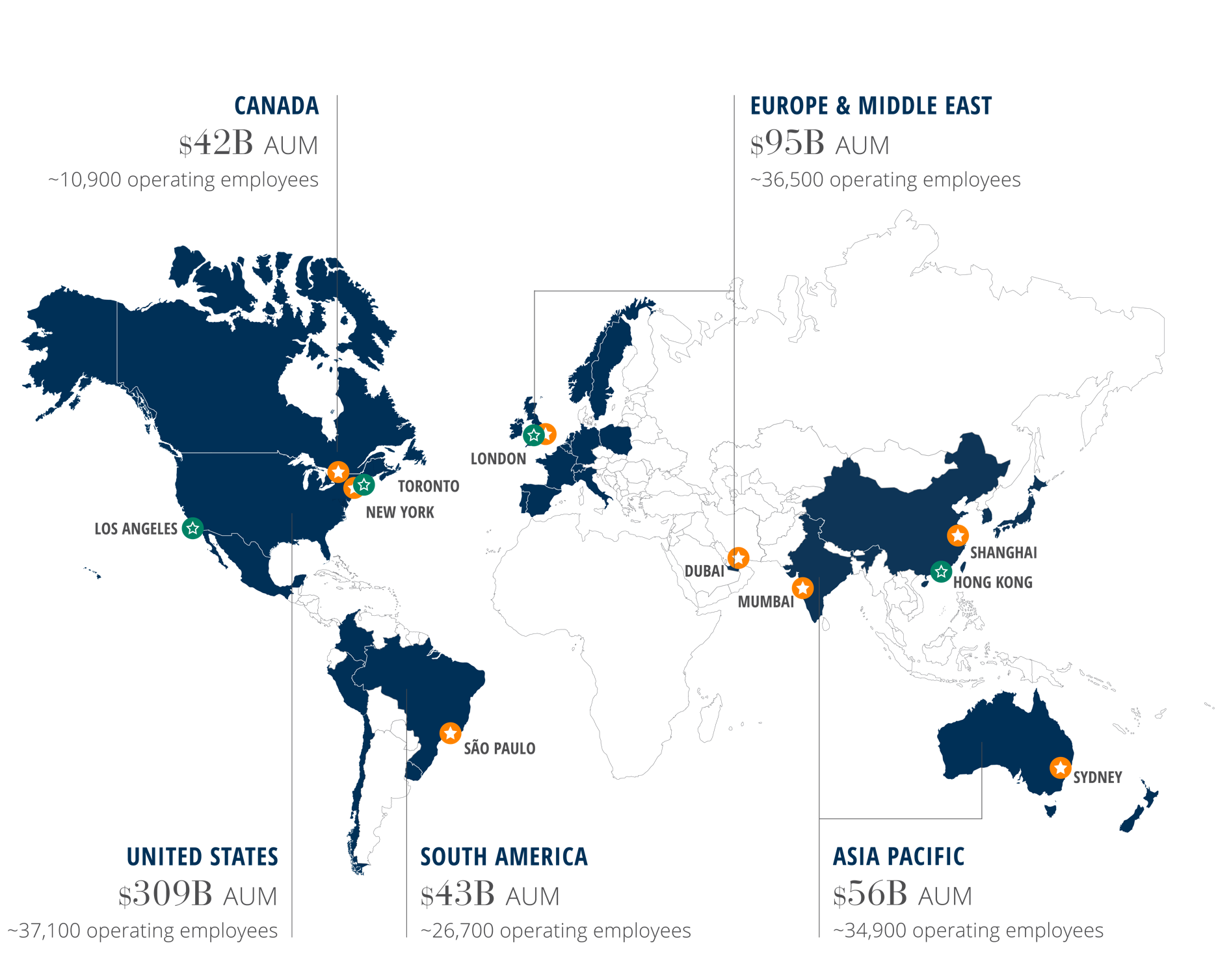

02Our Global Presence

Note: Excludes Residential Development and Corporate Activities which are distinct business segments for IFRS reporting purposes.

“Brookfield,” the “company,” “we,” “us” or “our” refers to Brookfield Asset Management Inc. and its consolidated subsidiaries. The “Corporation” refers to our asset management business which is comprised of our asset management and corporate business segments. Our “invested capital” or “listed partnerships” includes our subsidiaries, Brookfield Property Partners L.P., Brookfield Renewable Partners L.P., Brookfield Infrastructure Partners L.P. and Brookfield Business Partners L.P., which are separate public issuers included within our Real Estate, Renewable Power, Infrastructure and Private Equity segments, respectively. We use “private funds” to refer to our real estate funds, infrastructure funds and private equity funds. Please refer to the Glossary of Terms beginning on page 115 of our 2019 Annual Report, available for download above or here, which defines our key performance measures that we use to measure our business.

03Quick Facts

$540B+

Assets Under Management

$290B

Fee Bearing Capital

~1,000

Investment Professionals

30+

Countries

~150,000

Operating Employees

Core Investment Principles

Our approach to investing is disciplined and straightforward. With a focus on value creation and capital preservation, we invest opportunistically in high quality real assets within our areas of expertise, manage them proactively and finance them conservatively with a goal of generating stable, predictable and growing cash flows for investors and shareholders. Our culture is anchored by a set of core investment principles that guide our decisions and how we measure success.

Business Philosophy

- Build our business and all our relationships based on integrity

- Attract and retain high-caliber individuals who will grow with us over the long term

- Ensure our people think and act like owners in all their decisions

- Treat our investor and shareholder money like it’s our own

Investment Guidelines

- Invest where we possess competitive advantages

- Acquire assets on a value basis with a goal of maximizing return on capital

- Build sustainable cash flows to provide certainty, reduce risk and lower our cost of capital

- Recognize that superior returns often require a contrarian approach

Measurement of our Corporate Success

- Measure success based on total return on capital over the long term

- Encourage calculated risks, but compare returns with risk

- Sacrifice short-term profit, if necessary, to achieve long-term capital appreciation

- Seek profitability rather than growth, as size does not necessarily add value

Value Creation

We create shareholder value by increasing the earnings of our asset management activities and increasing the value of our Invested Capital, as follows:

Asset Management

1. Increasing fee-bearing capital, which increases our fee-related earnings. We track the value created by applying a multiple to our current fee-related earnings.

2. Achieving attractive investment returns, which allows us to earn performance income (carried interest). We measure the value created by applying a multiple to our target carried interest, net of costs1.

Invested Capital

3. Increasing the cash income generated by the investments as well as capital appreciation, through operational improvements and disciplined recycling of the underlying assets. We measure the value created using a combination of market values and fair values as determined under IFRS.

1. See definition in the Notice to Readers on page 19, of our 2019 Annual Report, available for download above or here.

2. Quoted based on December 31, 2019 public pricing.

3. Total IFRS invested capital excludes $4.9 billion of common equity in our Asset Management segment.

4. For business planning purposes, we consider the value of invested capital to be the quoted value of listed investments and IFRS value of unlisted investments, subject to two adjustments. First, we reflect BPY at IFRS values as we believe that this best reflects the fair value of the underlying properties. Second, we reflect Brookfield Residential at its privatization value.

5. Includes $2.2 billion of corporate cash and financial assets.

6. For the purposes of value creation, “current” carried interest, net represents target carried interest, net. Target carried interest, net, is defined in the Notice to Readers on page 19 of our 2019 Annual Report, available for download above or here.