Introduction

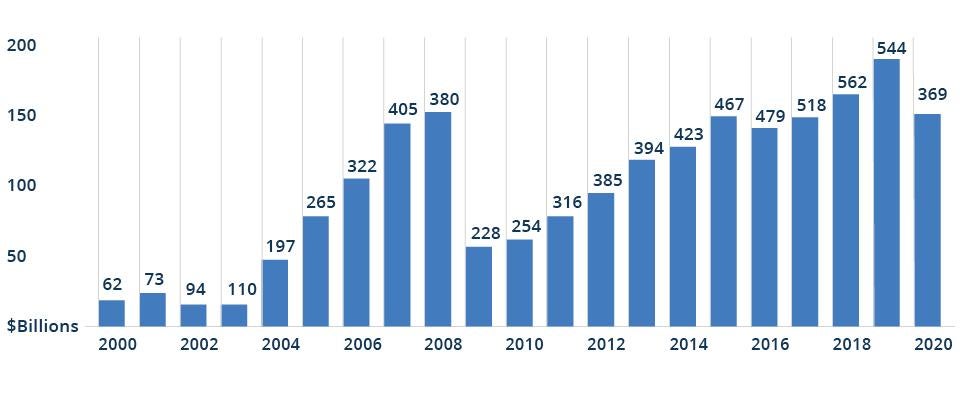

The growth of capital—both raised and deployed—by private equity real estate funds since the Global Financial Crisis has been impressive. More than $1 trillion has been allocated to such funds in the last 12 years.1 And both the growth rate—and the resulting quantum—do not appear to be slowing down.

As primary capital investments increase, a natural corollary market tends to develop in the form of secondary transactions. Simply put, secondaries are investments made in existing assets, structures or situations that bring fresh equity, reset an investment’s clock and re-align its ownership.

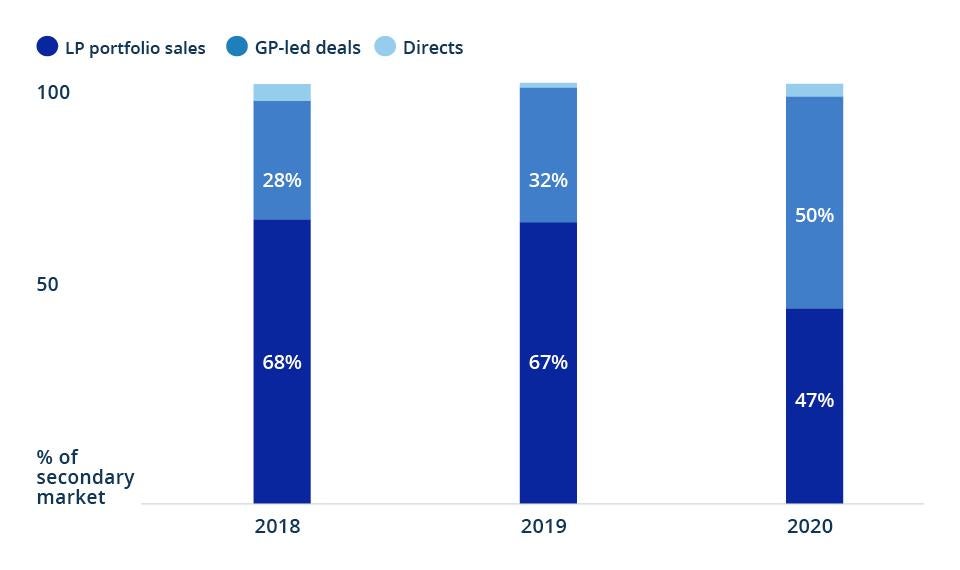

Real estate is an attractive corner of the secondary market, particularly given the advent of transactions known as GP-led recapitalizations. Once seen as a way to recapitalize assets that were difficult to sell, these transactions are now recognized by general partners (GPs) as an opportunity to hold onto their best assets. And for investors in these secondaries, GP-led recapitalizations often provide an opportunity to gain exposure to high-quality assets that were previously out of reach.

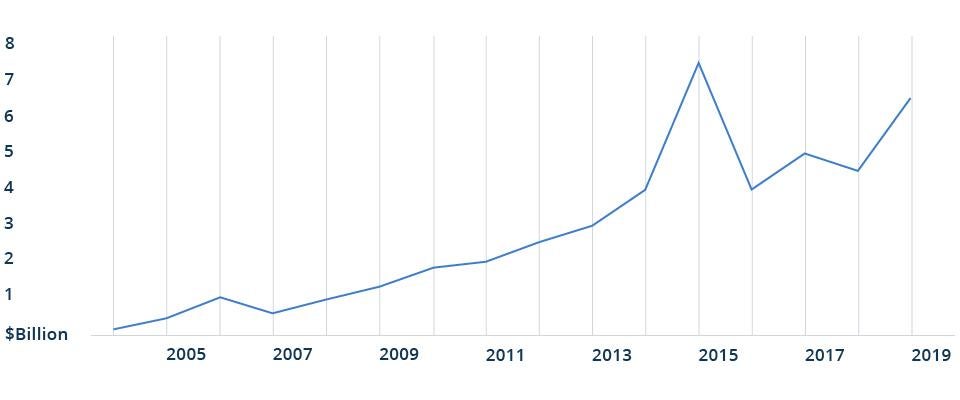

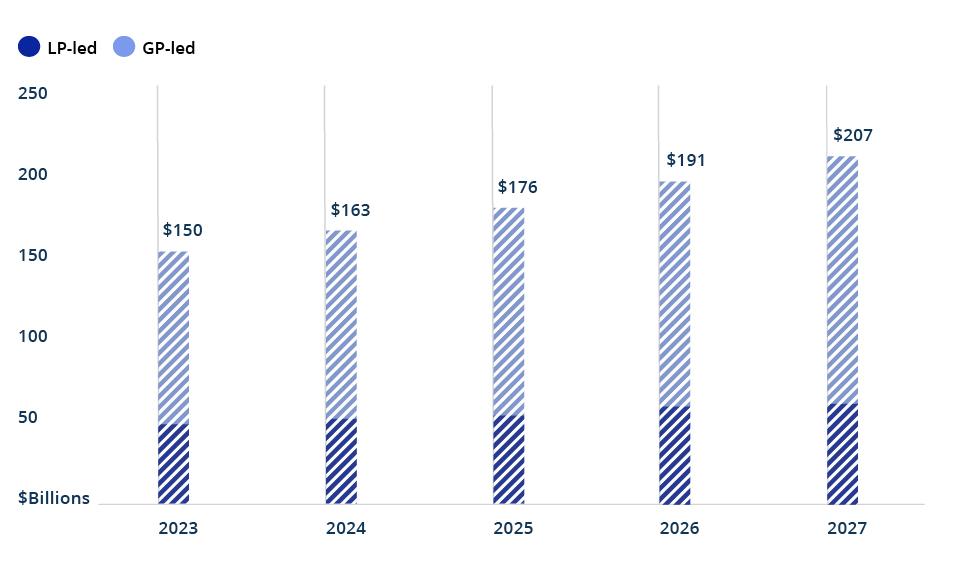

Indeed, real estate secondaries AUM reached 2.7% of all real estate AUM at the end of September 2020—up from less than 1% at the end of 2013.2 And we expect that ratio to continue to increase as more GP-led recapitalizations hit the market. Moreover, the investable universe is vast because almost any commercial real estate asset is a candidate for a secondary transaction, not just those in funds.

Yet, it’s important to remember that new opportunities can bring new complexities. As GP-led recapitalizations are quickly becoming the future of the real estate secondary market, we believe that making the most out of these opportunities will require specialized experience and expertise in owning, operating and investing in real estate.