White Paper

Building the Backbone of AI

Letter to Shareholders

Contents

Bruce Flatt

Chief Executive Officer

01Overview (as of February 11, 2021)

We ended the year with the best quarter on record. Given the environment and the extraordinary year, that says a lot for our business. Despite the turmoil and disruption, our investment strategies and the strength of our capital structure showed through. Results in our asset management business were very strong, with FFO up close to 20% over the previous year. Total FFO for the year of $5.2 billion was also a record, with realizations in the fourth quarter adding to results. On a go‑forward basis, annualized asset management revenues including carry are now running at $6.5 billion, and with our next round of fundraising for our private flagship funds just beginning, the franchise is poised for growth.

We have also launched four new strategies, and while none of these are expected to be significant contributors to our results in the short term, they should all be meaningful in the longer term. These include investing in LP secondaries, the energy transition to net-zero carbon, technology and reinsurance.

With respect to reinsurance, as recently announced, we plan to distribute to you a new share of Brookfield Reinsurance as a special dividend. This share will be paired with BAM shares to enable us to efficiently operate this business, and it should be attractive to some of you to hold.

Post year end, we launched a tender offer to take our property company private. We did this as most property securities trade poorly in the market, despite the underlying real estate being valuable. Taking it private will offer us greater flexibility in managing assets, and by paying our co-owners of BPY an attractive price, which they can elect to receive in a combination of cash, preferred shares with a coupon commensurate with current yields, or BAM shares for continued upside in the stock market, we believe it is best for all concerned.

02Bam Stock Market Performance Was Good, All Things Considered

As an indication of returns that can be generated for investors, below is our latest tabulation of annualized compound investment returns over the past 30 years. For reference, $1,000 invested 30 years ago in Brookfield Asset Management is today worth $86,000. Some years have been fantastic, some were like 2020; but as demonstrated in this table, compounding reasonable returns over long periods of time is an incredible miracle of finance.

The returns earned by a company are the reflection of many factors, but over the longer term they are the result of the combination of a good strategic plan and relentless execution of that plan. Only in the longer term is it possible to look back at both strategy and execution, which if done well, tends to also compound over time. Furthermore, we believe the intrinsic value of a Brookfield share today is greater than the share price; this gives us a large margin of safety in our efforts to record reasonable returns over the longer term.

03The Market Environment Was Unforgettable

Much has been said about 2020, and it surely was one of the most unusual years in memory. GDP in every country dropped precipitously, stock markets plummeted then recovered, central banks collapsed interest rates to zero, and money with little risk became virtually free. Many businesses were shut down, most worked from home, people were afraid, plane travel declined 98%, Brexit happened, and a new U.S. president was elected.

As the year turns over to 2021, markets are strong, borrowing costs are low, money is available to well capitalized borrowers, stock price multiples for many businesses are extremely high, and pharma companies have come through in amazing time with vaccines that are now being distributed. Our expectation is that economies will regularize as the at-risk populations are vaccinated, and as the death and hospitalization numbers decline. This is starting to happen now—albeit unevenly—and as governments and people get comfortable enough to resume a more normal life, we expect we will see a strong recovery in economic numbers starting now and into 2022.

With no meaningful inflation on the horizon and high unemployment numbers, there is an expectation that interest rates will stay low and that stocks that were not bolstered by the pandemic trade will recover. Other good companies that have elevated multiples either will be proven to deserve them, or their securities may trade sideways for a time, until their results catch up with their share prices.

Our operations are highly geared to the economic recovery. As a result, we should be able to grow the value of our businesses coming out of this recession while hopefully narrowing the gap between the intrinsic value and the trading price of a Brookfield share. Like most businesses, we are pleased to see 2020 behind us, and we look forward to 2021/2022.

04Our Business Was Strong, Despite Headwinds

During the fourth quarter, we generated a record $2.1 billion of FFO, an increase of 75% over the same period in 2019. Full year FFO was $5.2 billion, showcasing the resiliency of our underlying businesses. This is even more remarkable, as up to 20% of our businesses were shut for months during the year and some are still recovering. This should mean that as the global recovery takes hold, our results will get even stronger. All of this led to record total cash available to shareholders for distribution and/or reinvestment (CAFDR) of $3.1 billion or $2.01 per share in 2020.

Asset Management Performance was Good and is Getting Better

Our asset management franchise had a strong year in 2020. We increased total assets under management to $600 billion and fee bearing capital to $312 billion. Annualized fee-related earnings and target carried interest are now $6.5 billion on an annualized basis.

In total, we raised approximately $42 billion across our private fund strategies. This included capital for some of our flagship funds, and we also made great progress in raising capital for our perpetual core private fund offerings.

We now have approximately 20 different return strategies across our five main investment verticals that span senior debt to opportunistic equity. These included $13 billion of commitments for our latest distressed debt fund and $9 billion for perpetual core strategies. We also held a final close on our second infrastructure debt fund of $2.7 billion.

Despite the challenges of 2020, we generated approximately $1.2 billion of carried interest during the year and now have $4.7 billion of accrued unrealized carried interest on capital that has been invested. The benefits of the focus our funds have on critical service assets with contracted, leased or regulated cash flows were also highlighted in 2020, with valuations holding, and in some cases even increasing as a result of their income durability. We have re-initiated asset sales that had been delayed earlier in 2020, and demand for these assets has been strong. We recently announced a number of sales that we expect to close in the coming months; if they close as expected, 2021 should be another strong year.

At our Investor Day, we laid out our plans for the next round of flagship fundraising, with a target of $100 billion. Our flagship credit fund is off to a great start. We recently launched both our fourth flagship real estate fund and our new Global Transition Fund, which is focused on decarbonizing the global energy grid.

Operations Were Resilient

Our renewable power operations continued to deliver strong results in 2020, supported by a globally diversified asset base and long-dated, take-or-pay power contracts. During the year, BEP completed the privatization of TerraForm Power, and we recently announced the acquisition of a distributed generation platform in the U.S. Combined, these scale operations in solar, wind, hydro, storage and distributed generation position us well to participate in the decarbonization of the world’s energy supply.

Our infrastructure businesses were extremely durable during the year. With 95% of the cash flows backed by regulated or contracted revenue streams stemming from critical infrastructure assets, earnings were largely unimpacted by the economic shutdown. We continued to expand our investment in data, which is in a multi-year growth trend. We acquired a portfolio of 137,000 communication towers in India, which will capitalize on the rollout of 5G and other future technologies. We are also well positioned to participate in the global infrastructure investment and privatizations that are likely to follow as a result of both the sizeable debt that governments have taken on in recent months and their need to stimulate their economies.

Within our real estate business, most of our assets performed well in 2020. Our office portfolio is largely backed by long-dated leases to high-quality tenants, and rent collection was only marginally impacted. While our retail and hospitality assets faced challenges, in those markets where governments began slowly lifting restrictions, we have seen a steady rebound in performance. Foot traffic and sales per customer have increased significantly in our U.S. mall portfolio, and forward bookings for our hospitality assets are slowly recovering. During the year, we closed on the sale of a London office property, sold our U.S. self-storage business, and also disposed of a life sciences office portfolio—each well above both its acquisition cost and IFRS value.

Our private equity operations continued to grow, and we made a number of acquisitions, including a leading non-bank financial corporation specialized in commercial vehicle lending in India, and an Asia-based technology services platform focused on customer management services. We also announced the privatization of Canada’s leading mortgage insurer, and the merger of Norbord into West Fraser. We now own approximately 20% of this combined entity, which is the pre-eminent forest products business in North America.

Our credit platform delivered strong results in 2021. We were able to deploy $22 billion during the year, capitalizing on the March/April market dislocation, and other opportunities. We expect further opportunities to arise as government stimulus rolls off and companies need to recapitalize. The final close of our distressed debt fund is likely to take place in the first half of this year; it already is the largest distressed debt fund we have raised.

05Privatizing Our Property Business

In early January, we announced a proposal to acquire the balance of BPY that we do not already own. The simple story is that while the assets are exceptional and the tangible value is higher than the share price, property securities show no signs of trading near their intrinsic value. As a result, we believe our BPY partners will realize value far more quickly with the deal we are offering them.

Over the years, we have worked hard to execute our property business plans, with great success, but unfortunately the public markets have consistently struggled to appropriately value its assets. This is not unique to BPY; many property company securities have struggled to trade at NAV for years. In fact, we have taken private numerous real estate companies in our private funds for this very reason.

It has been evident to us for some time now that this portfolio and our approach to creating value are not well suited to the current public markets. To be clear, our view of the value of the portfolio has not changed. This is simply a classic example of assets not being what public market investors currently wish to invest into.

Privatizing the company will give us flexibility to realize the true value of the portfolio in the longer term by redeveloping some assets, constructing new ones, selling some assets outright, and using various assets to create or grow perpetual, private, core real estate funds. The conviction we have in the latter has been enhanced by our recent success with our series of perpetual private real estate funds that we now have in North America, Europe and Australia.

Although the immediate impact of the transaction will be an increase to the size of our balance sheet, this will quickly reverse, and we expect that over the next five years we will end up with fewer real estate assets than we have today—because of this transaction and the flexibility it will offer us. In time, we will also re-create the fee streams in the private markets, benefiting our clients who have a desire to own this highest quality real estate.

06The Next Beginning Has Already Begun

We are onto the next beginning for Brookfield. With all our funds performing well during last year, our balance sheets in extremely good financial shape, and our alternative investment management franchise now one of the pre-eminent businesses around the world, we are onto the next phase of growth for Brookfield. We have widened the moat of our business globally and continue to add new products for our clients. With interest rates low, alternatives are the investment category that offers an attractive return for our clients, and we are innovating to provide them with new products.

We are also scaling up the size of our large flagship funds. Their size differentiates us and therefore enhances our returns. In addition, our clients are looking for income replacement with less volatility, and we are continuing to add perpetual core-plus products to our platform.

New areas of focus for us are investing in the transition of the economy to net-zero carbon emissions; reinsurance; technology investing, where we are moving from venture into full-scale technology private equity investing; and LP secondaries, where our clients are increasingly looking for scale managers. Each of these areas has the potential to provide a meaningful opportunity for our clients and for our business.

07Climate Transition to Net Zero Is Real and Accelerating

As we have noted for many years, overall, Brookfield is already net negative on scope 1 and 2 across our entire $600 billion of assets under management on an avoided emissions basis. We believe we are similarly net-zero carbon on a scope 3 basis and are now measuring the scope 3 emissions of our portfolio companies in detail. Having transformed our own business from a very intensive generator of carbon decades ago to net-zero carbon today, we believe we are well positioned to assist others with this change.

With decades of expertise and the access to capital that we possess, we plan to raise capital from our clients to assist other companies in moving to net-zero carbon. We are committing over $2 billion of our own capital to our Global Transition Fund and will be investing that alongside institutional clients who are like-minded in their goals. We believe this represents a unique opportunity to create a new asset class while addressing one of society’s current greatest needs.

We believe the world is at the beginning of a 30-year movement to net-zero carbon. This transition will affect virtually every business in every country. China, currently one of the largest generators of electricity from coal, has recently committed to being net-zero carbon across its entire economy before 2060. The new U.S. administration has committed to clean energy by 2035, and the EU, the U.K. and Canada are all accelerating their energy transitions. There is now no disputing that the world overall is moving from fossil fuels to lower carbon energy—renewables, nuclear energy and potentially hydrogen.

Within the envelope of net-zero carbon, we will continue to own and operate certain essential infrastructure assets globally that transport fuel. We believe that natural gas will play an important role in this energy transition, particularly in Asia, and potentially serve as a bridge to hydrogen. Rest assured, when we acquire these assets, we will be laser focused on the duration of cash flows, and we will operate them with their contributions to the transition to net-zero carbon in mind and with plans to ensure they continuously do better. We believe the operating experience we have gained in transitioning from carbon-intensive to net-zero carbon ourselves will make us better owners of many of these assets.

Our Global Transition Fund is focused on the build out of new renewables globally, as well as the operations surrounding investment by businesses to accelerate the transition to net-zero carbon. There are many companies that will have the capital and skills to do this themselves. Equally, there will be many that need our operating expertise and access to capital to achieve their goals. This is the objective of our new fund, and we are excited about what it can accomplish.

08A Few Themes Are Driving Our Investing in 2021/2022

We invest in all of our businesses to maintain and grow them, but we seek to deploy the most capital in businesses or regions at opportunistic points in time when the opportunity to create greater incremental value exists. This changes constantly, but simply stated, we try to stay away from fairly valued markets and invest where capital is in short supply.

Our investing is also driven by themes that generally cross all of our funds and are longer term in nature. The themes that we believe are relevant for our business today are as follows:

- Low interest rates will continue to drive demand for alternative investments. Interest rates appear to be set to stay in a lowish band for several years. As a result, alternatives are very attractive to investors. This provides an exceptional backdrop for our overall business.

- Renewable energy is growing. The global electricity make-up is currently 25% from renewable sources, and this is set to grow to 50% or more over the next 30 years. The investment required to accomplish this is in the tens of trillions of dollars.

- Technology is affecting all business, as it always has. The difference today is the pace of change, which brings with it great opportunity, but also risk. We are embracing this.

- Alternative credit is here to stay. Capital from institutions and reinsurers will increasingly drive the credit markets. Alternative managers have the opportunity to scale up credit as a fixed income replacement for institutional investors.

- Most real estate withstood the dramatic shutdowns in 2020, and while some property will be used in new ways in the future, there will be no major paradigm shift. Great real estate in great cities will continue to be just that. This will become evident once the global economy recovers.

- Many businesses and governments require capital. While businesses have survived thus far by borrowing heavily, they now need equity. As a result, there will be attractive opportunities to invest in businesses, and to acquire infrastructure from governments.

09Our Partnership Approach

Lastly, we encourage you to focus on our business, not the share price. If there was ever a year to emphasize this point, it was 2020. Consider that the Price of BAM in US$ on a split adjusted basis, started the year at $38.58 and ended the year at $41.27. With a dividend of 1.25%, you earned a respectable 8% on your investment based on the share price. Except, given the extremes in the market seen in 2020, and depending on when you looked at the Price, you might have concluded that you had gained 18% if you looked in February, or a month later that you were down 44% when our shares traded at $21.57 in March. This is the behavior of Price; but not Value.

In the short run, Price is a function of supply and demand at any point in time, which is often influenced by the news of the day, short-term results, and the investor view of macro events that often have nothing to do with the company. This has always been true, and is even more so today with the emergence of ETFs, indexing, social media, the 24‑hour news cycle and all the information bombarding investors. Value, on the other hand, is the net present value of future cash flows based on assumptions for growth, discounted back to the present at an appropriate interest rate. The Price of a publicly traded security is very often not the Value of it; sometimes it is higher, and sometimes lower. From time to time they can converge—but not that often.

The Value of Brookfield based on our published plan value metrics was $57 at the start of 2020 and $66 at the end. After accounting for the dividend, your Value increased 17% over the year. This was very respectable, especially given the environment, and it included write-downs from some businesses that got hit in the short term with the shutdowns.

If we were a private company, we would simply report our Value calculation and the metrics behind it. You would likely have been thrilled with 2020. We actually were. On the other hand, the movement of Price often distracts investors from focusing on the Value of a business. We encourage you to focus on Value and try to not be distracted by Price.

10Closing

We remain committed to being a world-class asset manager, and to investing capital for you and the rest of our investment partners in high-quality assets that earn solid cash returns on equity, while emphasizing downside protection for the capital employed. The primary objective of the company continues to be to generate increasing cash flows on a per-share basis, and as a result, higher intrinsic value per share over the longer term.

And do not hesitate to contact any of us should you have suggestions, questions, comments or ideas you wish to share.

Sincerely,

Bruce Flatt

Chief Executive Officer

Note: In addition to the disclosures set forth in the cautionary statements included elsewhere in this Report, there are other important disclosures that must be read in conjunction with, and that have been incorporated in, this letter as posted on our website at https://bam.brookfield.com/en/reports-and-filings.

Brookfield at a Glance

01Our Business

We are a leading global alternative asset manager with $600 billion of assets under management, and a focus on investing in long-life, high-quality assets and businesses that help form the backbone of the global economy. Our goal is to enable the companies and assets we invest in, as well as the communities in which we operate, to thrive over the long term.

We serve a broad range of institutional investors, sovereign wealth funds and individuals around the world. As stewards of the capital our investors entrust to us, we leverage our experience and deep operating expertise to create long-term value on their behalf, helping them meet their goals and protect their financial futures.

Our capital structure is built to allow us to finance investments by drawing from various sources—including our own balance sheet, our publicly listed affiliates’ capital and capital from our institutional investors. This access to flexible, large-scale capital allows us to pursue transactions for our investors that are significant in size, generate attractive financial returns and cash flows, and support the growth of our asset management activities. Importantly, it also means that our capital is invested alongside that of our investors, ensuring that our interests are always aligned with theirs.

At Brookfield, sound Environmental, Social and Governance (ESG) practices are integral to building resilient businesses and creating long-term value for our investors and stakeholders. These practices are routed in our philosophy of conducting business with a long-term perspective in a sustainable and ethical manner. This means operating with robust governance and other ESG principles and practices, and maintaining a disciplined focus on embedding these principles into all our activities.

Our people remain the most important element of our business, and our culture is based on integrity, collaboration and discipline. We place a strong emphasis on diversity across all our businesses, because we recognize that our success depends on fostering a wide range of perspectives, experiences and world views.

Investment focus

We focus on real estate, infrastructure, renewable power, private equity and credit.

Diverse product offering

We offer core, core-plus, value-add, opportunistic/growth equity and credit strategies through closed-end and perpetual vehicles in both the public and private markets.

Focused investment strategies

We invest where we can bring our competitive advantages to bear, leveraging our global reach, access to large-scale capital and operational expertise.

Disciplined financing approach

We take a conservative approach to the use of leverage, ensuring we can preserve capital across all business cycles.

Sustainability

We are committed to ensuring that the assets and businesses we invest in are set up for long-term success, and we seek to have a positive impact on the environment and the communities in which we operate.

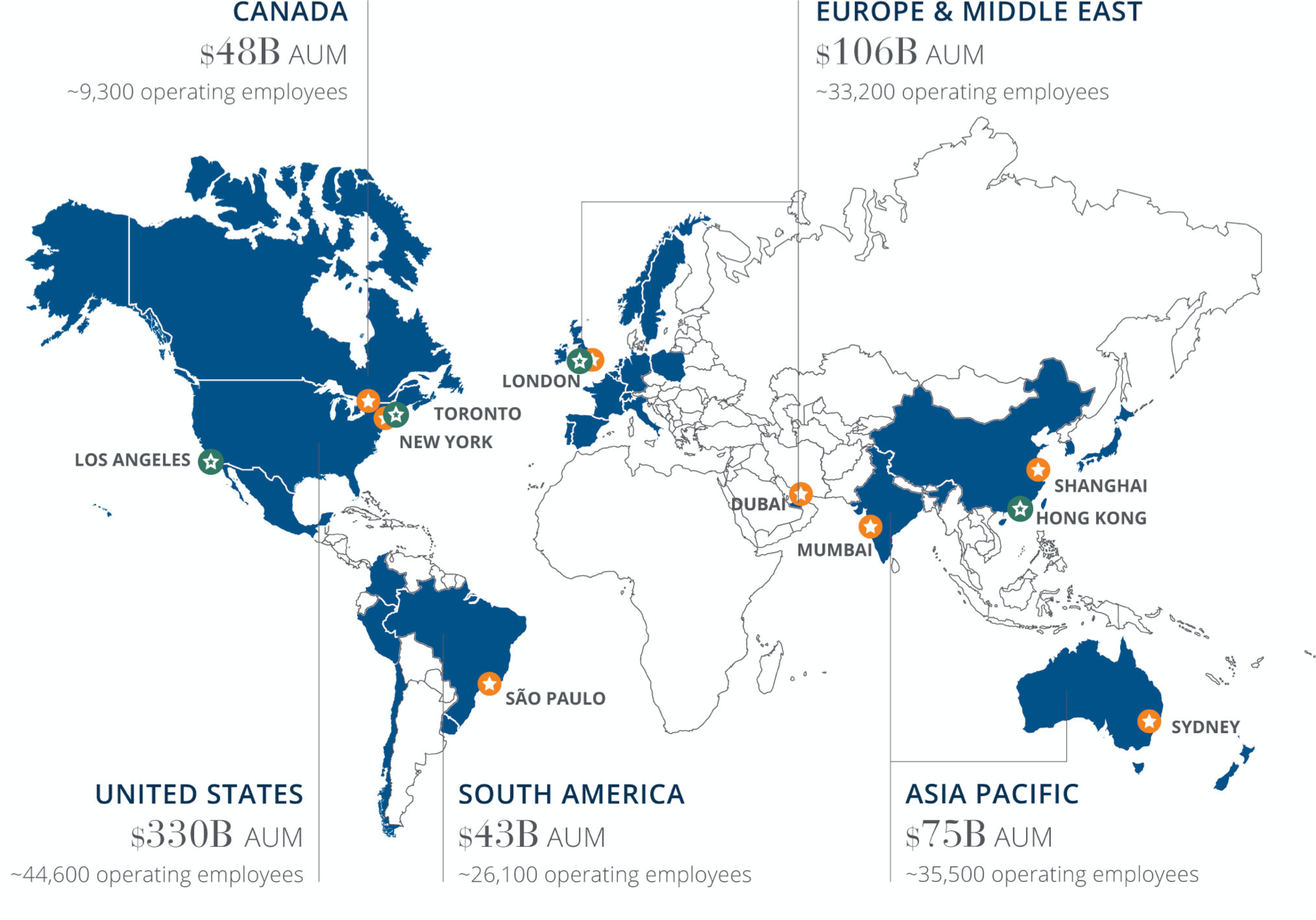

02Global Reach

“Brookfield,” the “company,” “we,” “us” or “our” refers to Brookfield Asset Management Inc. and its consolidated subsidiaries. The “Corporation” refers to our asset management business which is comprised of our asset management and corporate business segments. Our “invested capital” includes our “listed affiliates,” Brookfield Property Partners L.P., Brookfield Property REIT Inc., Brookfield Renewable Partners L.P., Brookfield Renewable Corporation, Brookfield Infrastructure Partners L.P., Brookfield Infrastructure Corporation and Brookfield Business Partners L.P., which are separate public issuers included within our Real Estate, Renewable Power, Infrastructure and Private Equity segments, respectively. We use “private funds” to refer to our real estate funds, infrastructure funds and private equity funds. Please refer to the Glossary of Terms beginning on page 115 which defines our key performance measures that we use to measure our business.

03Quick Facts

$600B+

Assets Under Management

$312B

Fee Bearing Capital

~1,000

Investment Professionals

30+

Countries

~150,000

Operating Employees

Exchanges NYSE: BAM TSX: BAM.A

Investment Principles

Our approach to investing is disciplined and proven—reflecting our more than 100-year history as an owner-operator. We focus on value creation and capital preservation, investing opportunistically in high-quality assets and businesses within our areas of expertise, managing them proactively and financing them conservatively—with the goal of generating stable, predictable and growing cash flows for all our investors. We recognize that generating attractive risk-adjusted returns often requires taking a contrarian approach to evaluating assets, businesses, markets or sectors.

Our business is anchored by a set of core investment principles that guide our decision-making and determine how we measure success:

Business Philosophy

- Operate our business and conduct our relationships with integrity

- Attract and retain high-caliber individuals who will grow with us over the long term

- Ensure our people think and act like owners in all their decisions

- Treat our investor and shareholder money like it’s our own

- Embed strong ESG principles throughout our operations to help us ensure that our business model is sustainable

Investment Approach

- Acquire high-quality assets and businesses

- Invest on a value basis, with the goal of maximizing return on capital

- Enhance the value of investments through our operating expertise

- Build sustainable cash flows to provide certainty, reduce risk and lower our cost of capital

Measurement of our Corporate Success

- Evaluate total return on capital over the long term

- Encourage calculated risks, but compare returns with risk

- Sacrifice short-term profit, if necessary, to achieve long-term capital appreciation

- Seek profitability rather than growth, as size does not necessarily add value

Value Creation

We create value for our shareholders by increasing both the value of our Asset Management franchise and of our Invested Capital, as follows:

Asset Management

1. Increasing fee-bearing capital, which increases our fee-related earnings. We track the value thereby created by applying a multiple to our current fee-related earnings.

2. Achieving attractive investment returns, which enables us to earn performance income (carried interest). We measure the value thereby created by applying a multiple to our target carried interest, net of costs.1

Invested Capital

3. Increasing the cash income generated by the investments as well as capital appreciation, through operational improvements and disciplined recycling of the underlying assets. We measure the value thereby created using a combination of market values and fair values as determined under IFRS.

1. See definition in the Notice to Readers on page 15.

2. Quoted based on December 31, 2020 public pricing.

3. Total IFRS invested capital excludes $4.9 billion of common equity in our Asset Management segment.

4. For business planning purposes, we consider the value of invested capital to be the quoted value of listed investments and IFRS value of unlisted investments, subject to two adjustments. First, we reflect BPY at IFRS values as we believe that this best reflects the fair value of the underlying properties. Second, we adjust Brookfield Residential values to approximate public pricing using industry comparables.

5. Includes $4.5 billion of corporate cash and financial assets.

6. For the purposes of value creation, “current” carried interest, net represents target carried interest, net. Target carried interest, net, is defined in the Notice to Readers on page 15.